Factor investing has the potential to offer up tangible investment opportunities while maintaining a healthy range of diversification within the portfolios of investors.

This strategy has received increasing levels of popularity thanks to the choice investors have in buying into securities on attributes that can promise consistently higher returns.

The two primary factors that continually drive healthy returns on stocks, bonds and other forms of investment are centred on macroeconomics and style factors. In the case of macroeconomics, broad risks are captured across various asset classes while style factors focus on explaining returns and risks within asset classes.

Investors keen on embracing factor investing have plenty of choice as to where their focus can be. Common opportunities to be found generally include the variable factors of credit, inflation and liquidity when it comes to macroeconomics, and that of style, value and momentum within the field of style-based factor investing.

But what does factor investing actually entail? And how practical is it when looking at how to best build a portfolio? Let’s take a deeper look at the ins and outs of factor investing:

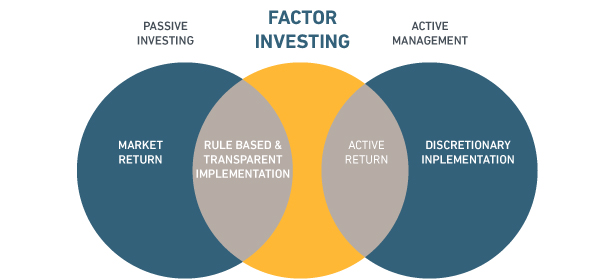

Factor investing in a nutshell

Theoretically speaking, factor investing is structured to uphold the commonly accepted practice of diversifying portfolios, while generating greater returns from investments and managing risk effectively. The form of diversification upheld by factor investing attempts to ensure the safety of shares – all while protecting investors better from losing the potential gains they could be achieving by utilising the more frugal holding method.

Image Source: MSCI

We’re always advised to diversify our bonds, but one prospective downside to this approach is that the gains associated with diversification can often be lost if the invested securities move in lockstep with the broader market. This means that even if you have a high performing asset, your profit margins will be mitigated by a widespread decline of your other assets. As so many investments are heavily conditioned by the same external factors, oftentimes declines are exponential across all assets held within a portfolio.

Traditional portfolio applications are relatively simple in their allocation – with ratios like 60% stocks and 40% bond distributions in the offing. The fact that factor investing is much more complex than this approach can ultimately seem off-putting for interested parties. This is primarily down to the wealth of factors to choose from and base your portfolio around.

The more rudimentary approaches to factor investing can, justifiably, build portfolios based on style elements like growth vs value, or size such as large-cap vs small-cap assets as well as risk (in the case of smart beta).

The factors above tend to be readily available for analysis on many popular stock research websites, but the decision-forming factors that can enter the fray when it comes to factor investing doesn’t stop there, and some investors can become considerably meticulous in identifying investment opportunities.

Opportunities for higher profit margins

It’s fair to say that factor investing is an ambitious approach that’s designed to effectively optimise the potential of profits without neglecting the need for diversity within portfolios. As a result, there is little margin for error when picking the prospective assets that would hold the most value for investors. Luckily, Investopedia has constructed a strong list that covers the ‘foundations’ of factor investing that we can delve into and expand on:

Firstly, the foundation of value is intended to capture returns emanating from stocks that are priced outstandingly low compared to their perceived interpretation of worth. This can commonly be tracked by price-to-book, price-to-earnings, dividends and free cash flow.

Size can play a significant role in bolstering the value of portfolios. Traditionally portfolios built on small-cap stocks return greater profit margins than those of only large-cap stocks. This tactic can be used by factor investors by taking a look at the market capitalisation of any specific stock.

Another significant influence comes in the form of momentum. Stocks that have previously built up ahead of steam can often show strong returns moving forward. Momentum strategies are also typically grounded, relatively speaking, in tangible returns within a three-month to a one-year timeframe.

Quality can be defined by things like low debt, stable earnings, consistent growth and even strong corporate governance. All experienced investors are on the lookout for quality assets, and many use metrics like return-to-equity and debt-to-equity ratios to identify the best contenders for their portfolio. Additionally, earnings variability can aid investors’ abilities here.

The foundational principle of volatility doesn’t sound like a very solid one, but empirical research shows that stocks with lower levels of volatility can earn much better risk-adjusted returns than that of highly volatile assets. This may seem logical but it can be hard to conclusively identify. However, investors can measure standard deviation from a one-to-three year timeframe to gain the best insights into the volatility of a potential asset.

Upholding the rules of diversification

The perceived beauty of factor investing is its potential for bringing strong returns while minimising your portfolio’s risk by upholding the well-accepted safety net of diversity.

The fundamental reason why factor investing and portfolio diversification go hand-in-hand is down to how different factors are capable of covering a wide range of scenarios and are thus likely to perform well in different economic areas. This means that if one of your investments is underperforming, the chances are that others will still be doing well – because of the fact that they’re nestled in a completely different industry.

This enables factors to act as a driving force when it comes to minimising the usual risk associated with investments. Another way factor investing helps to pave the way for better returns is through the opportunities of encompassing specific asset traits that are historically proven to produce high and consistent returns.

Due to investors possessing the ability to isolate the traits that they’re more interested in, a strong ‘smart beta’ strategy can involve choosing a portfolio based on these perceived strengths across the board. Furthermore, some investors even choose this type of portfolio as a way of complimenting their traditional index funds – this is because factor investing helps to mitigate market exposure and boost the levels of market coverage within periods of volatility.

Dangers of market bubbles

The notion of optimised and diversified assets that are based on a pre-determined set of desirable factors seems like something of a pipedream, and in some cases, it can be.

It’s fair to say that factor investing is an excellent way of making tactical investments through a smart beta strategy, and theoretically, it’s a revolutionary way of building portfolios that follows on from the famous ‘Moneyball’ approach towards player recruitment in baseball – where Billy Beane enjoyed great sporting success after hiring his playing staff based on the analysis of less conventional attributes and stats.

However, invariably a catch or two follows on from such revolutionary financial ideas. Just like the brilliance of Moneyball flourishing for Beane until his rivals began to adopt similar approaches, factor investing has become a victim of its emerging popularity.

Already, Wealthsimple has reported that the key issue of factor investing today is not so much the logic behind the strategy, but the fact that multiple investors are focusing on the same metrics in a bid to inform their decisions. This collective gold rush for desirable factors has pushed up the prices of some assets with desirable qualities beyond its true value – this naturally eats into the future returns that investors can expect to see.

Another major problem with factor investing comes in the form of complacency. Because there is a perceived safety net of diversified assets, those investing in factor-based strategies struggle to retain the big picture when finding the right opportunities.

By dedicating your hunt for valuable assets based solely on specific criteria, there’s a strong possibility that you’ll miss out on attaining a healthy, well-balanced portfolio. There’s the additional risk that the assets you purchase may not always offer the factors that made you invest in them in the first place – meaning that you may be forced to refresh your assets more often than usual.

The art of the long game

Despite there being risks associated with the longevity of the assets you hold in your portfolio when adopting a factor investing strategy, this isn’t to say that investors should adopt a more short-term mentality when holding their shares.

On the contrary, factor investing is certainly a more long-term strategy that requires plenty of patience and a stiff upper lip.

Depending on the type of factors you choose to focus on, your portfolios could endure prolonged periods of underperformance or stagnation. This can be an extremely dangerous aspect of life for less-experienced traders, who may be frightened by the prospect of seeing their assets fall further and thus decide to sell.

If you’re trigger-happy with assets and unwilling to endure periods of poor performance, then there’s a strong possibility that you’ll sell up at the wrong time and thus receive below-market returns on your investments – immediately undermining your entire strategy.

Be sure to exercise patience and trust your portfolio. If you’ve done your homework, diversified the assets that you’ve bought into and homed in on factors that you believe will guarantee their long term security – then you have the best chance of being awarded for your faith.

![How Options Trading Works: The Ultimate Guide [2021]](https://daglar-cizmeci.com/wp-content/uploads/2020/12/Options-Trading-400x250.jpg)