Over the 25 years, the topic of intergenerational wealth will continue to gather momentum as the Great Wealth Transfer takes hold. Throughout this time, the Baby Boomer generation will pass down a total wealth of as much as $68 trillion to inheritors in what will be the largest transfer of wealth in history.

The coming decades will be a challenging time for wealth management firms and their advisors, as their familiar clientele will begin to reach retirement age and begin to pass on their assets to children, grandchildren and younger friends and family.

Generational wealth is a topic that there’s no getting away from, and advisors will need to adapt quickly as more wealth starts to change hands. Here’s a deeper look at the pros and cons for wealth management firms choosing to gain a footing atop the shifting sands of generational wealth:

Pros

1. Embracing the Great Wealth Transfer

The irresistible force of the Great Wealth Transfer is coming, and it holds plenty of opportunities for wealth management firms willing to modernise and turn extra focus onto services pertaining to intergenerational wealth.

Next of kin, children and grandchildren are set to receive an unprecedented volume of wealth, and will likely do so as one bulk payment. This seismic change in asset ownership can certainly be regarded as a positive for advisors.

With a new set of clients comes a new series of financial objectives. In the slowing property market of today, reduced DB transfer figures and expectations of a coming recession – inheritors are more likely than ever to seek out the help of wealth management firms to navigate the tricky landscape.

This could result in a substantial shift in the level of assets under the management of financial advisors and thus rejuvenate the industry of wealth management.

2. Flexibility in transferring wealth

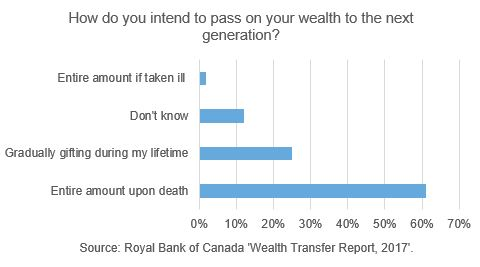

(Image: Russell Investments)

The chart above illustrates a hefty benefit for wealth management companies as we enter the age of the Great Wealth Transfer.

The notion of passing down wealth is considered a taboo subject for many asset holders due to the topic’s connotations of death and illness – but generational wealth doesn’t have to start at the end of life.

Almost two-thirds of respondents to Russell Investments’ survey surrounding intentions on when to transfer wealth to the next generation claimed they would do so upon their death, while 12% stated that they haven’t decided what to do when it comes to the passing down of their assets.

It’s estimated that there are as many as 76 million Baby Boomers approaching retirement age in the US alone. With over 60% risking the pinch of Inheritance Tax by transferring their wealth upon death accompanied by 12% who don’t know what they’ll do, advisors are looking at a market of over 50 million individuals who may benefit from wealth transfer advice.

3. The opportunity to promote inheritance planning

The Great Wealth Transfer is the ideal opportunity for wealth management firms to focus on promoting inheritance planning.

For ambitious and scaling wealth management companies, it could pay dividends to start looking today at how to engage with clients about the importance of effective inheritance planning, and the significant benefits that can be found in transferring wealth within their respective lifetimes.

The conversation surrounding inheritance will continue to gather momentum as the ‘Boomer generation continues to approach retirement age and as a result, your business and its advisers will invariably attain plenty of clientele by moving early and allocating resources to accommodate the arrival of this mass market. From a scaling perspective, there’s no better way for a wealth management firm to strategically expand.

Cons

1. Changing industries and attitudes

Naturally, the widespread disruption that generational wealth will cause over the time of the Great Wealth Transfer will come with its fair share of cons alongside the opportunities it creates.

Over the coming decades advisors, clients and banks will change significantly along with respective client risk profiles. It’s already clear that the notion of intergenerational wealth and its connotations aren’t openly discussed in families, and gaining client insight on this matter will oftentimes prove tricky.

There’s also the difficult transition between existing clients and their younger benefactors. Growing up in the wake of the 2007 financial crash has made Millennials relatively cautious when it comes to the spending of money. As many of these younger generations receive new and larger sums of wealth, life experience may fundamentally change their views on how to invest – thus challenging advisors to adapt to new wants and needs in a very short timeframe.

Advisors will also need to think about how alined their current clients’ investment propositions are with that of future clients. Here it could be beneficial to take a well-rounded stance. By engaging with inheritors early on, you will be setting yourself up with a head start.

Depending on the generation that the inheritors find themselves in – whether it be the ‘sandwich generation’ that has their own parents and children to support, or younger generations – it’s important to keep adaptive.

Your future clients will have different goals and desires. Some will want to fund or repay their education, while others could be more focused on house deposits. The best course of action would be to discuss these matters with benefactors directly along with existing clients to see if their objectives can be addressed at an earlier stage.

2. The burden of inheritance tax

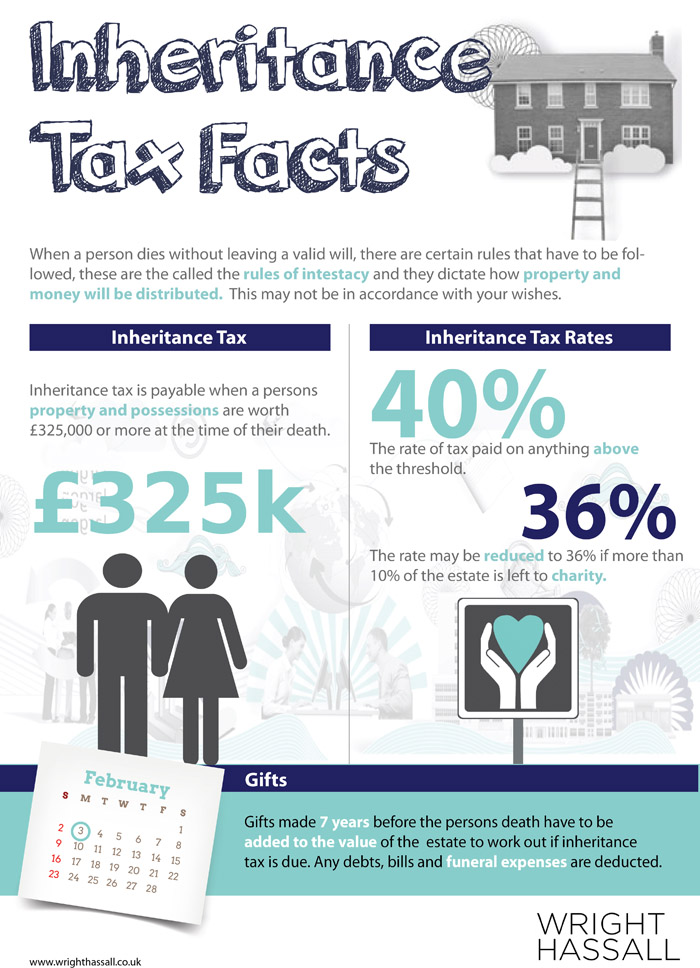

40% can seem like a hefty percentage. This is the figure that Inheritance Tax stands at today in both the US and UK, though the percentage rate fluctuates around the world.

(Image: Wright Hassall)

Whether your clients are in favour or against this divisive form of taxation, it will significantly reduce the volume of capital available for new clients to invest. This, in turn, means that new clients may have just 60% of the wealth of their predecessors ready to invest.

It will undoubtedly be a challenge for the wealth management industry to continue to encourage inheritors to invest their wealth following the pinch of taxation and advisors will need to adapt their approach to provide all the transparency and financial education required to guide new clients through this process and optimise the opportunities available to them.

3. Poor client retention

The problem with Millennials is that they’re something of a fickle generation.

According to Victor Preisser, co-founder of the Institute for Preparing Heirs, “over 90% of heirs promptly change advisers when they receive their inheritances, and 70% of families lose control of their assets when an estate is transitioned to the next generation.”

Such figures will no doubt appear daunting for wealth management firms. Losing inheritors is one thing, but losing them after spending time building rapport with their family means an air of familiarity is lost also.

The solution to this problem lies in making efforts to modernise your processes. Embrace alternative communication methods like live chatting and non-face-to-face contact. It’s also advisable to invite clients to talk about the topic of generational wealth with their families. This will not only help advisors to gain an understanding of prospective inheritors’ objectives but will also provide a great opportunity to build rapport.