As the age of information has given people an array of tools to plan and manage their wealth, it can sometimes be difficult to navigate what is right for you. The access to information and advice given to you about what to do with your money can turn into wealth planning and financial goals overload, and this isn’t the most productive feat either. More often than not when it comes to wealth planning, simplicity is key. You can align your finances with a basic plan and go from there, the key is consistency and longevity.

What is Wealth Planning?

Wealth Planning is the understanding that your finances will offer different things to you at different stages in your life and serve you in different ways. By implementing a financial plan for yourself, you will in theory be paying your future self by prioritising what you want your wealth to do for you. Whether it be planning for your retirement or managing your wealth portfolio, you can hire external help in the form of a wealth manager or you can very much manage your finances yourself and ensure that you’re keeping your financial goals on track.

When it comes to savings and establishing what you should prioritise first, can often be what causes problems later down the road when it comes to wealth planning. In America alone, just under half the population have no savings which highlight that setting financial goals and planning where you want your wealth to go will be something that your future self will thank you for.

(Image Source: Statista)

Worry Less, Plan More

When it comes to the essentials of planning your wealth and setting financial goals for yourself, you need to be able to let go of the outcomes that you can’t control. It doesn’t sound like an intuitive step when it comes to wealth planning, but it’s important to establish this before even delving into the meaty bit of your finances.

What is realistic for you when it comes to your finances? How many sources of income do you have and how much of this can you be saving or investing? By being honest with yourself, you can begin to divide your wealth into tangible goals and start your wealth plan. When being bombarded with social media and articles about how people have become millionaires within a short period of time, this is not realistic for most people. There is no one amount that makes you rich and by gaining a sound understanding of this, you can realistically and objectively manage your finances. Everyone’s situation is different so worrying over a finite number that may not even be applicable to you is taking away from making the most out of your income and financial situation.

So rather than putting all your concerns into how much you think you should have within a certain time, look at your finances as they stand and how you think you can divide them. This is a great time to set your financial goals and establish what you want from your money.

Financial Goals

Now that you have the mindset of being ready to plan your wealth, creating financial goals for yourself is primary for your money and assets. If you are a beginner at planning your wealth, you must first outline what your wealth actually is. Do you own property? Do you have an emergency fund? Are you looking into investing your money? Create a document, or even on a piece of paper, and list all your accounts and how much money you have in each one, and this way you will have an overall picture of what you are working with.

Before you begin to outline your financial goals, you have to ensure you have an emergency fund. Whether you’re a millionaire or just starting out your first paid job, managing wealth is being as in preparation as you can be with your money. An emergency fund can simply be at least three months’ worth of your living expenses, ideally in a high yield savings account.

Once this is done, you can figure out how much debt you have and what you want to prioritise paying off. Is it in your best interest to pay your credit cards first or your loan? By referring to what you outlined earlier, you can focus your attention on what needs to be done with a matter of urgency.

After this, you can begin to outline what percentage of your income you want to put into savings spending and investments. The easiest way to work with your current income is in percentages. Can you put 15% of your monthly income into savings and still have enough to cover your essential expenses? Work out how much you can put towards your future savings and how much you want for your own personal spending each month. If you work in an industry or working style that doesn’t have a set income every month, then split your year up into financial quarters and go from there. By working in percentages you are working alongside what you have without fixating too much on the numbers.

Once your basic financial needs are met you can then begin diversifying your wealth and planning further with what you want to do with your income.

Cleanse Your Spending

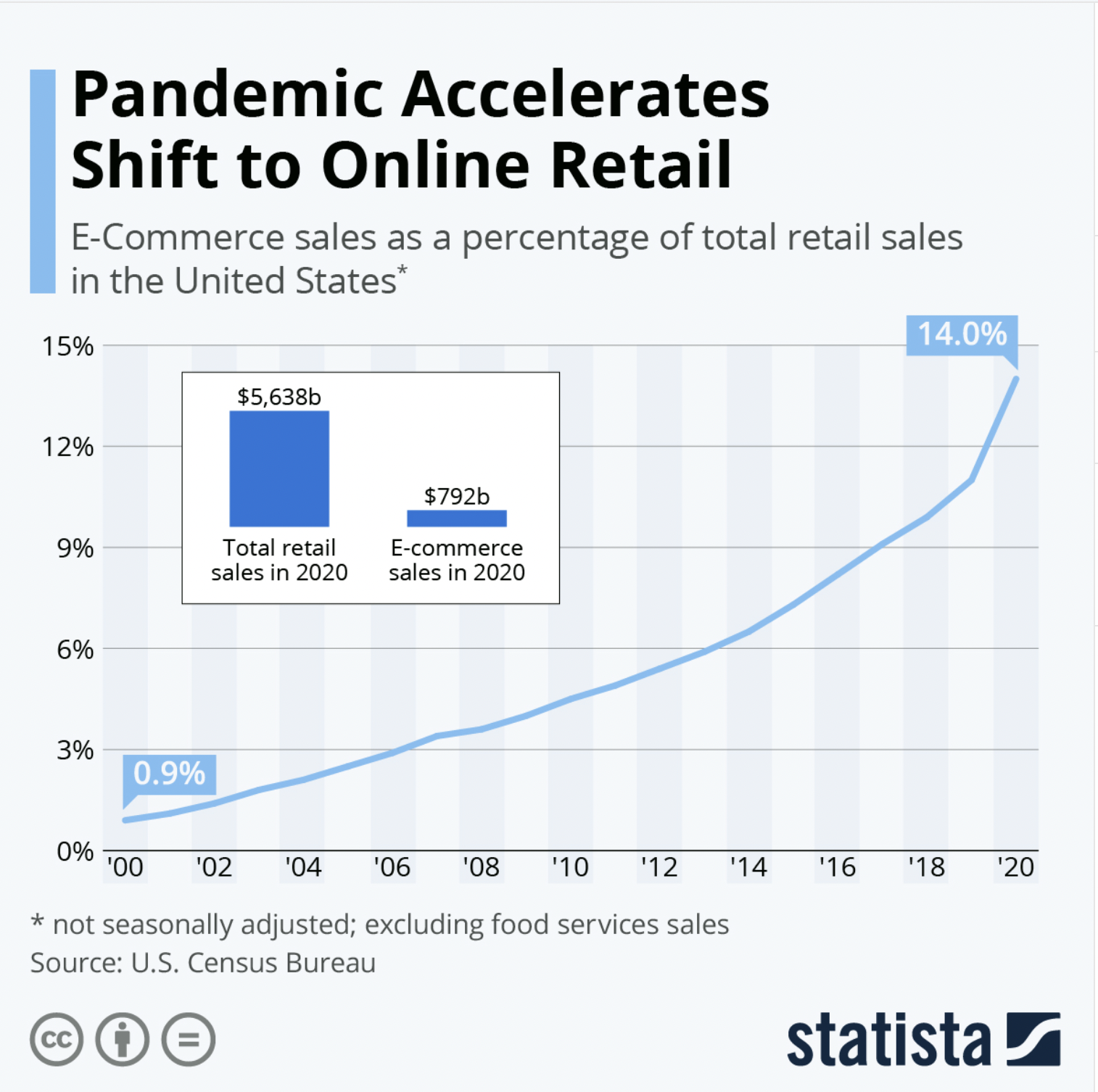

When it comes to outlining your incomes you must do the same with your outcomes. Be honest with how much you are spending your money and where. The pandemic has facilitated a lot of online spending and sometimes encourages purchases that we don’t necessarily need. Being aware of your spending and purchases may be the very thing that you need to do to get on top of your finances.

(Image Source: Statista)

When actioning a cleanse in your spending, being clear on your monthly outgoings (such as subscriptions, investment payments, and direct debits) will put you in good stead to see what you do and don’t utilise, from here you can cut down your subscriptions and see what you use the most. Financial Educator Tori Dunlap suggests having a money date with yourself. Try essential spending for a set period of time and consider putting the extra money into savings or towards your emergency fund.

Pay Yourself First

It can be tempting to wait until the end of the month to see what you have left and then put that into savings, but in order to be organised with your money, you have to pay yourself first. This does not mean going out and splurging on material items, but putting money towards your future self. This could be your retirement fund, your investment account, or money towards a property. These should have consistent payments in order to make them worth your while and leaving your money to reap the benefits of the account that you put them in will be great for your future. Going back to percentages is what will help you here too. What percentage of your money needs to go to your essentials, then how much can you spare for your future self?

Saving as much as you reasonably can, can feel less active with the beauty of automation. Automating what goes into your savings accounts and into your funds on the say that you get paid, means that you’ve paid yourself before you’ve even had a chance to miss that money and what’s left in your account is what you’re left to work with.

Diversification of Your Investments

We’ve been told since we were little that saving is a good thing, which of course is important when it comes to establishing a financial plan, but ensuring that you include diversity is crucial. With the current financial climate, the yield that is given from savings accounts is at an all-time low, so many people are turning to invest as a way to save for their future. When speaking about diversification in the financial sense, essentially meaning not putting all your eggs in one basket when it comes to your money. With regards to diversification, this can be in regards to how you save or money and how you choose to invest your money.

When choosing to invest your money, there has to be an empirical awareness that you are putting your money at risk. Just as your investment can make you money, it can also use your money, which is why it is important to establish a range of ways in which you are investing. This could be in the form of different stocks and shares or property as an investment. Diversification of the way you distribute your money should be considered as your safety net when it comes to investing. Well, as safe as you can get when it comes to investing.

If you are not an investment expert there are now a range of means that you can seek help to ensure you are investing in ways that work for you and that you are happy with. Whether this is in the form of financial advisors to manage your wealth or assets or using apps to keep track of how often you would like to invest, deciding how you would like to invest should be a part of your wealth planning and considered when it comes to your financial goals. You should not consider investing if you do not have the capital to put up for the risk. If you are taking a complete gamble when it comes to your investments, you should prioritise where your money needs to go first of all and consider investing as something that comes following paying off your debts. When it comes to the diversification of your investments, time is your biggest asset. The earlier you can start investing the more you are likely to benefit from it, so starting small is something you ought to consider. Establishing what is a realistic amount for you to start investing should be outlined when you initially write down your current financial situation.

Spend Below Your Means

Speaking about wealth planning and finance, the word budget is not one you can escape. After outlining your financial goals, having a budget will help you stay on track with your financial goals. When it comes to anything outside of saving, you should limit yourself and try to spend within your means, and keep your costs low.

The first point of the call is to make sure your credit cards are being used to your advantage. Are the purchases you are making on your credit card because you really need to make that purchase, or are you spending outside of your means? Some examples of when it’s good to use your credit cards are when making larger purchases and by using your credit card, you have an element of protection there and build up your credit score at the same time. Credit cards are a great tool to have in your financial repertoire and by factoring regular use of one into your financial plan, you could get more back for yourself and be smart with your purchase. For example, investing in a credit card that offers air miles and you travel a lot is good for you because you are getting something back for your spending. Research is key when it comes to deciding how you will spend your money, so look into the credit card that offers the best deal for your lifestyle and start there.

If you are in the infancy of your finance and wealth planning, doing your research and going that extra mile to keep your costs low will help you overall with future planning. Shop around and see when it is the best time of year to make a purchase, can you hold off on luxury household expenses until they are on sale, or could you ensure that you are getting the best possible deals on your bills? By putting in that little bit of effort and time, you could be saving yourself a good amount of money.

Multiple Sources of Income

When it comes to wealth planning, there are simple steps you can do to create additional ways of making money for yourself. If you work in the traditional sense and get paid by an employer, can you think of other forms of income that can supplement you without you given up a significant amount of your time? The ways that people are working are now more varied than ever, and if your job allows you to work remotely, you could utilise the time it would normally take for you to travel to put into a side hustle.

Establishing a secondary source of income for yourself is definitely something you should consider for your financial plan. This could be passive or active income, but not relying on one source of income is key to reach any financial goals you may have. Passive Income is setting up a situation for yourself in which money is made without you exchanging your time for money. This could be in the form of a rental property or selling merchandise online or could even lie in reselling clothing. It’s a great way to add to your financial goals and to consider as part of your wealth planning. Active Income is being paid relative to the amount of time you work, this is typically what you action when you work a full-time job on an annual salary. This could be picking up a part-time or weekend job, or offering online services such as virtual assistance.

If part of your wealth planning is establishing multiple sources of income for yourself, you need to think about the steps you need to take to make that happen. If you want to save and invest in a rental property, what accounts would be best for your to implement to make it a reality for you? What money would you need to put aside and implement into your financial planning to prioritise this for yourself?

When it comes to multiple sources of income you may already be at the stage where you have established this for yourself and you need help in managing them. Part of your financial plan may be knowing when to start factoring in the help you need. Outsourcing the management of your assets will not only free up your time but the peace of mind in knowing that your investments are being taken care of. If you are in a position to manage your assets yourself and this is where your expertise lies, then you should do what you feel the most comfortable with, but if more time is something that you want to achieve and include in your wealth plan then outsourcing is something you should most definitely consider.

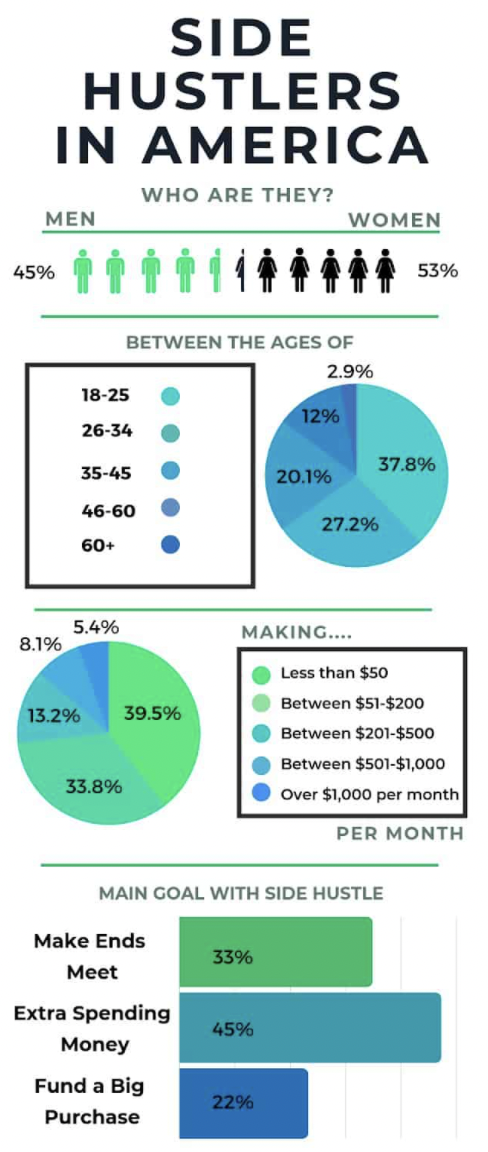

(Image Source: Dollar Sprout)

Plan For Tomorrow

Retirement is something that not many people think about until they are later in their life, but it is something that needs to be considered in your wealth planning. Creating a nest egg for yourself is dependent on how much retirement is a priority in your life and if you would like to retire early. If you have a time that you would like to be retired by, then you must navigate and work your finances towards that. You can use retirement calculators to work out how much you would need to put away to comfortably live within a certain amount of time and take into account all of your investments and assets.

When working for an employer, you can use the pension scheme that has been made available to you with your company and pay into your pension straight from your paycheck. More often than not your company will match your contribution and even when you move jobs, you will still have that nest egg, that will become available to you. Alongside this, you can create a private pension and include this in your wealth plan. You can go through wealth specialists to do this, or speak to your bank and see what kind of long term accounts will be good for you and your retirement plan.

Long Term vs Short Term

Wealth Planning is something that needs to be addressed annually as your financial goals are bound to change and be adapted to your financial situation. Creating long term and short term financial goals will allow you to cater for your current financial situation with your future goals and wants.

A short-term financial plan can run from 3-5 years. This comes off the back of outlining your financial wants in general and establishing their longevity. For example, if you want to build a property portfolio as a long-term goal, what can you implement in your short term financial plan to begin to achieve that? Think about the area where you would like to begin purchasing property and look into how much you would be willing to spend and what you would like to put down as a deposit, then from this, you can create an annual budget for yourself and what you would like to save towards that goal in the short term. With a long term financial plan, you can think ahead, like with retirement and how long you would like your investments to mature. Thinking in the long term will allow you to break down your financial goals into smaller and more manageable chunks.

With wealth planning, there is a lot to consider and research when establishing what it is you want your money to do for you. The way that the current economy is, being resourceful and thinking outside of the box when it comes to your finances will help your money flourish. Creating financial goals and thinking about the future will give you clarity on the basics of wealth planning and reduce the probability of getting stuck in a financial rut. Being financially prepared will give you a safety net and even allow you to explore other financial avenues and factor them into your wealth plan.