The best way of capitalising on your spare money is through saving or intelligent investing. When it comes to savings, you have plenty of options. You could create a savings account, a checking account or certificates of deposit. While there’s no right or wrong answer as to which approaches are the best for your needs, your circumstances and timeframes towards seeing a return on your investment may see your needs change.

The biggest benefit of creating savings accounts is that you have to deal with limited levels of risk when it comes to losing the value of your investments. With more stock-based investments, however, your capital is at more risk, but you have a much better chance of making significant passive earnings.

There are plenty of different forms of investment out there, and as the world faces a testing era of financial fallout from the devastating emergence of COVID-19, value investments are becoming much harder to come by. To help you better navigate the testing economic landscape here’s a range of various approaches to investing that have been proven in the past. As we move into the 2020s, it’s becoming clear that the new decade will be full of new challenges in growing our wealth, so let’s take a look at some of the most significant ways of wisely looking after our money:

1. High-Yield Online Savings Accounts

Sometimes success can be found in keeping things simple. Just like the types of savings accounts that you can find in your high street bank branch, high-yield online savings accounts are highly accessible and promise relatively risk-free returns on your invested wealth.

With lower levels of overhead costs, it’s possible to earn more money in interest online than through brick and mortar banks. Despite COVID-19 uncertainty, there are still many banks available offering over 1.5% in interest rates online.

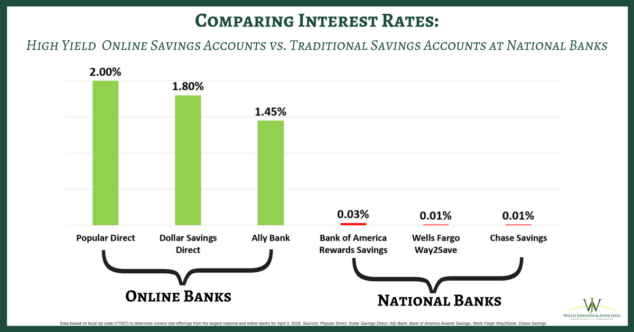

(Image: Willis Johnson & Associates)

As the chart above illustrates, online savings accounts have the power to eclipse those offered by established high-street banks. Savings accounts are also great if you’re looking to access your funds in the not-too-distant future. Whereas other investment methods could involve locking away your wealth for years to come.

Of course, there are risks involved with taking out high-yield online savings accounts. However, the banks that offer these types of accounts are typically FDIC-insured – which means that there should be no danger of losing your initial deposit.

One of the most significant things to take into account with high-yield accounts is that while they’re generally considered as safe investments, you do risk earning less when it comes to reinvesting your money due to inflation.

The greatest perk of opening a high-yield online savings account is the high liquidity involved. In most cases, you can freely add or remove your savings at any time. This is particularly useful as we enter into a recession that could see a greater level of market unpredictability as a result.

2. Investing in Real Estate Investment Trusts (REITs)

REITs take the form of real estate investments made as a direct investment on a property, known as Equity REITs, or by taking a mortgage out on a property, known as a Mortgage REIT. It’s also possible to partake in a more hybrid approach that combines both Equity and Mortgage REITs.

REITs can be taken out with a single property, or it’s possible to spread your risks out by investing in various properties and locations. Diversifying your portfolios is a golden rule within investment and the same can apply to property investments too. The demand for specific properties within different locations can vary based on a wide range of different factors, so a wider portfolio can take this into account.

REIT investors can receive dividends and various tax benefits for their portfolios, making it a relatively low-risk investment that could yield enviable returns. IT can also guarantee a regular income. Furthermore, the housing market isn’t directly affected by the whims of the stock market, meaning that there’s less risk involved in REITs.

3. Nasdaq 100 & FTSE 100 Index Funds

An index fund based on the Nasdaq or FTSE 100 is an ideal choice if you’re an investor who wants to find some exposure to some of the biggest and brightest tech companies without having to go to the hassle of researching the growth of individual companies and their stocks.

These finds are based on the Nasdaq and FTSE’s 100 largest companies, which means they’re the most successful and stable organisations based in the US and UK respectively. The esteemed list will include industry giants like Microsoft and Apple, among other leading innovation specialists.

This form of stock market investing enables investors to gain an instant level of diversification, so that your portfolio won’t hinge on the performance of a single asset and company. The best Nasdaq and FTSE funds charge low expense ratios, which means it’s a cheap means of owning a high volume of companies populating the index.

Of course, it’s worth remembering that all stocks can move down as well as up, and because the top 100 performing companies domestically will be the highest valued, there’s always the chance that their shares can become overprices and subject to quick falls in times of recession. However, they’re also more likely to recover faster when economic recovery begins.

Conveniently, Nasdaq and FTSE index funds can typically be converted almost instantly, meaning that you’ll maintain a healthy level of liquidity should you need to access your investments sooner rather than later.

4. Rental Housing

If you have the time to invest in the upkeep and management of multiple properties, buying property to let out can be one of the most steady and secure long term investments that can be made.

Of course, to utilise this as a viable approach towards making money, you will need to possess enough wealth to find an attractive property and finance it or buy it outright. More built-up areas and university towns are particularly useful areas to let out your properties to students and young people yet to get onto the property ladder.

Sadly, while this form of investment is reliable, it involves plenty of research and hands-on work. You’ll need to be prepared at all times for things to go wrong, pipes to burst and refrigerators to fix.

But the great thing about letting out property is that you can generate a significant passive income well into your retirement, meaning that you can ensure a continuous long-term cash flow that doesn’t take long to cover short term losses from property acquisition.

The last financial crisis showed that housing could be in a bubble that’s ready to burst, and if you’re looking for liquidity, this probably isn’t a method for you. However, if you continue to monitor the geographical, demographic and economic environments surrounding the property you plan to invest in, it’s possible to make some very shrewd purchases that will continue to appreciate over time.

5. P2P Lending

Peer-to-Peer lending is an investment tool that can allow individuals to lend from other parties instead of taking out a bank loan. To facilitate this, the two parties meet on Peer-to-Peer sites that essentially matchmake borrowers and lenders alike. The sites then act as mediators in setting terms and conditions of borrowing and a loan is brokered. The website Prosper is particularly effective in setting up the right lenders with borrowers.

At its best, P2P lending represents a win-win situation for both investor and borrower. Lenders can offer cheaper interest rates for the borrower while they themselves make much more money than what they would have if it were left to lay in a standard savings account.

Naturally, there are higher levels of risk involved in this form of investment, and while it’s an excellent way of generating a passive income, borrowers may default on their repayments – leading to heavy losses. However, well-regulated investor platforms are effective in mitigating these issues – limiting the risk held by lenders. However, this investment doesn’t involve the highest level of liquidity.

6. Certificate of Deposits

Certificate Deposits act as investments where banks set interest rates to be paid to specific investors over a pre-determined period of time. The investor receives their arranged returns if they don’t attempt to access their money during said period. This low-risk form of investment works similarly to a savings account, but with a lower level of liquidity. This enables banks to use the money to invest in their own endeavours, allowing investors to earn greater levels of interest on the funds they deposit.

If the pre-determined agreement is undermined by the investor, their interest will be significantly reduced. Returns on their investment will be wholly dependent on the Certificate of Deposits period and the interest rates that were agreed. However, despite being an investment that pretty much forces investors to be locked in for a prolonged period of time, interest rates are usually significantly higher.

7. Money Market Accounts

Money Market Accounts are typically an FDIC-insured, interest-bearing deposit account that promises higher levels of interest than your typical savings accounts but require higher minimum balances to be opened.

Due to their higher levels of liquidity and better yield levels, Money Market Accounts are a strong and safe option for rainy day savings.

However, for better interest, users tend to have to agree to more restrictions on the withdrawals they make, which can sometimes severely limit the access you have to your money.

One of the biggest risks to Money Market Accounts comes in the form of inflation. If inflation exceeds the interest rates that you’re earning on your account, this could severely undermine your investment.

While Money Market Accounts are considered liquid, regulations in place can force account owners to lower the number of withdrawals they make to a maximum of six per month, for instance.

8. Dividend Stock Funds

Stock market investments are typically regarded as more volatile than a lot of the options within this list, however, with stock market funds that pay dividends, you can ensure a greater degree of safety for your portfolio.

In a nutshell, dividends are a percentage of a company’s profits that can be relayed to shareholders – typically on a quarterly basis. With dividend stocks, you can earn on your investments through standard market appreciation but also short term injections of finance in the form of dividends.

It’s worth noting that any form of stock-based investments will come with a significant level of risk, and regardless of whether you stand to receive dividends on high-performance quarters or not, there’s always a chance that you’ll lose money as well as make money. With this in mind, it’s perhaps worth spending a prolonged amount of time studying the markets before dipping your toes in.

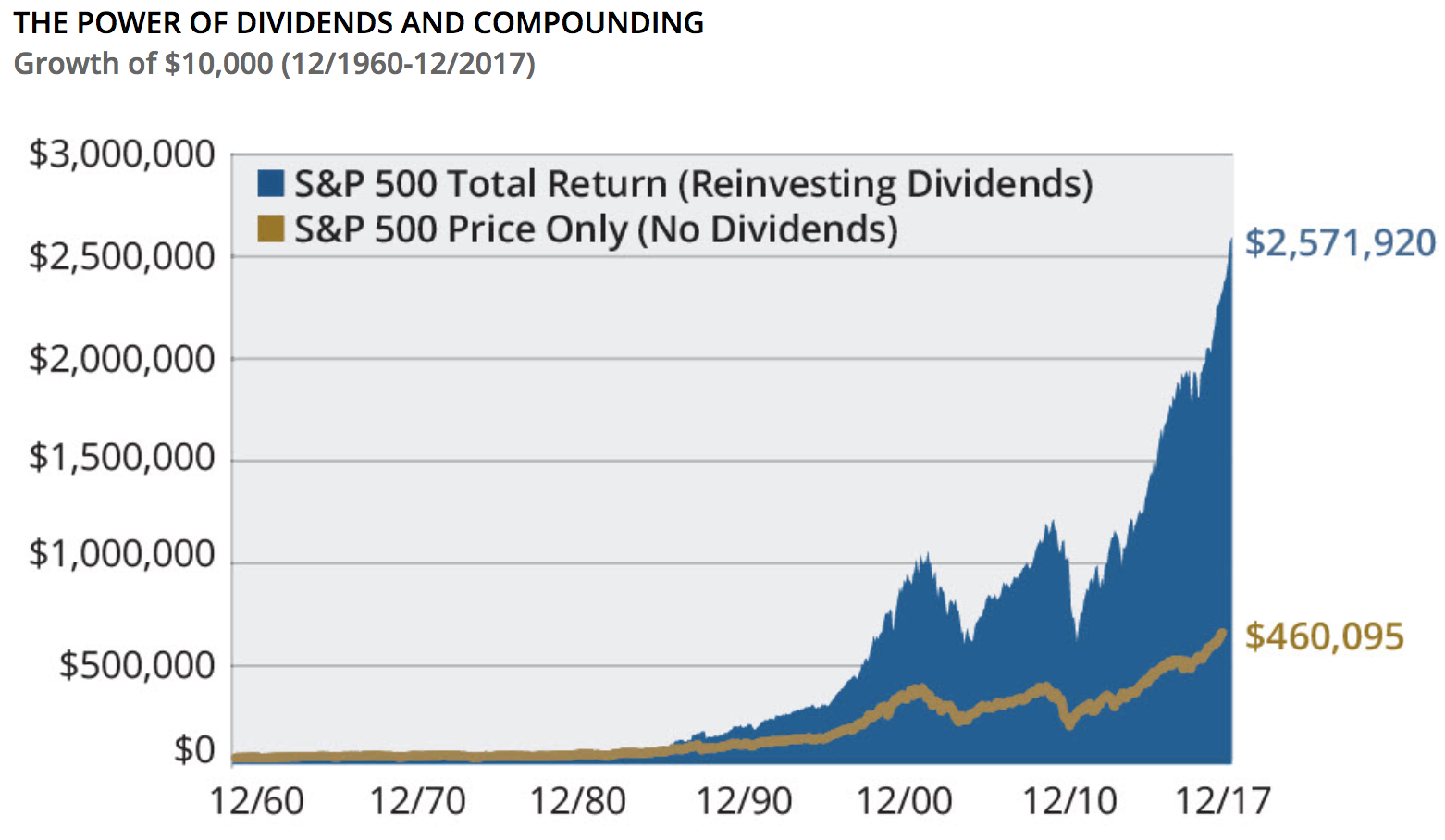

(Image: Simply Safe Dividends)

The chart above illustrates the level of growth that an investor could see if they invested dividends stocks and re-invested their dividends over a prolonged period of time.

Liquidity remains high for this form of investment and the dividends themselves are typically paid in cash – meaning instant liquidity. However, to get the most out of dividend stocks, it’s certainly worth playing the long game, and so you may have to leave your money alone to see the true benefits.

9. Short-Term Corporate Bonds

Some corporations choose to raise revenue by issuing bonds to prospective investors. This can help more casual investors to gain exposure by buying into bonds that have a maturity of between one and five years – helping to keep them immune to future interest rate fluctuations in the longer term.

The great thing about Corporate Bond Funds is that they can help investors looking to build their cash flow within a lower-risk portfolio while maintaining a healthy level of returns.

The risks posed by this investment approach is that you’re putting your faith into the performance of the issuing company. If the endeavour fails or faces a downgraded credit rating, there’s a chance they’ll default on their bonds – leaving you with a loss on your investment.

However, the short term nature of these bonds means that they have a better level of liquidity, and it’s possible to sell and reinvest your funds at any time.

10. IPOs

Initial Public Offerings represent a company’s way of securing shares listings on securities exchanges. An initial offer is made to the public, enabling them to subscribe to the share capital of a company at an introductory price before it becomes part of the secondary market allowing more investors to trade.

An IPO doesn’t necessarily ensure that would-be investors receive shares, but because they’re such an early opportunity to get involved in investments, there are great opportunities in shares doubling in value for a business with high potential. However, there’s also the danger of making heavy losses if said company doesn’t reach its potential.

11. Municipal Bonds

Particularly popular among US-based investors is the Municipal Bond. These play the role of debt securities that are offered by governmental bodies where money needs to be borrowed for local development.

The great thing about Municipal Bonds is that they earn interest on a tax-free basis, and the chances of the borrower defaulting are extremely low. It also gives investors a chance to earn a reliable stream of income while investing in their own city or region.

Readily available to buyers, Municipal Bonds are issued with serial maturities and represent a near-guaranteed level of return.

12. Investment Apps

One of the fastest-growing developments of recent years comes in the form of fintech apps and micro-investing services.

Apps like Moneybox help users to save while they make small purchases – whereby rounding up their morning £2.50 coffee to £3 and investing the 50p change on their behalf, for instance.

Money-saving apps help to provide users with a form of passive savings where the money is squirrelled away in small, virtually unnoticeable amounts, automatically invested with a pre-determined level of risk and yield depending on how adventurous the investor is, with portfolios and investment fluctuations transparently made available for users to see.

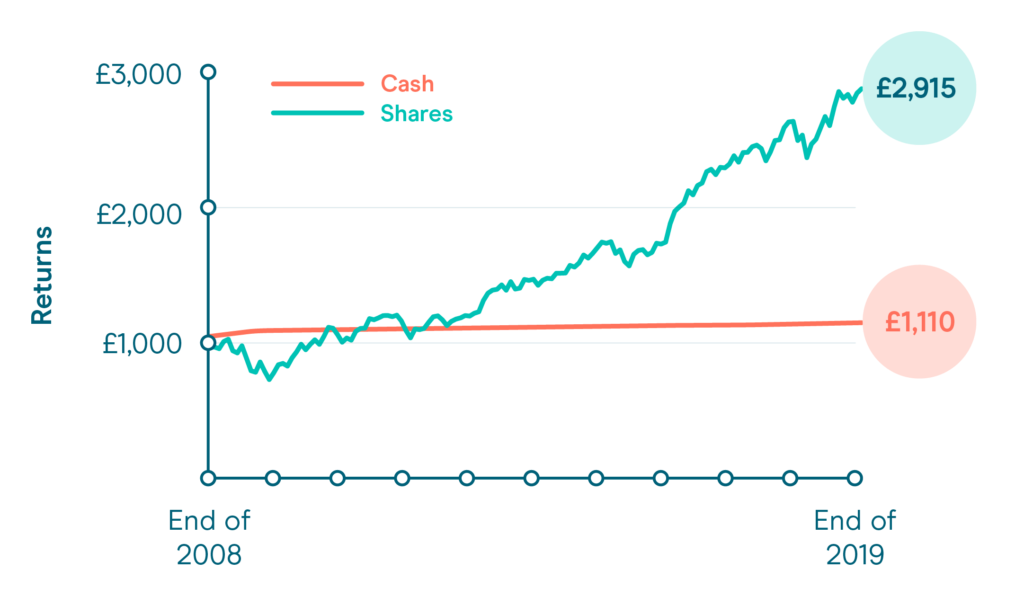

(Image: Moneybox)

According to their own figures, Moneybox estimates that users investing through their app could have nearly tripled their profits in the wake of the 2008 financial crisis. However, with the arrival of the post-COVID-19 recessions worldwide, the performance of automatic investments may yet cause worrying fluctuations in performance.

In terms of liquidity, investments are easy to take out of your money-saving apps and convert into ready-to-use money – however, depending on the type of ISA you take out with the app some access can be harder to gain.

13. Corporate Bonds

No Corporate Bonds are created equally – which makes them rather difficult to summarise in a matter of two paragraphs. Fundamentally, Corporate Bonds are classified as high, medium, or low quality. They are typically issued by large companies to finance new projects and expansions into fresh markets with the promise to pay a fixed interest to investors over a pre-determined period of time.

It’s worth noting that Corporate Bonds are riskier than Municipal Bonds because they don’t have the same level of governmental backing – there’s also no tax exemptions on the interest earned. However, it may be easier to access corporate bonds with more generous levels of interest depending on the level of research you undertake.

14. Preferred Stock

Preferred Stock is a form of Capital Stock besides the Common Stocks that companies tend to issue to investors. While Common Stocks come with shareholder voting rights, this privilege doesn’t concern Preferred Stockholders.

Despite this, Preferred Stocks provide investors with their money as a priority ahead of Common Stock investors. Also known as Hybrid Securities, Preferred Stock possess a par value that’s affected directly by interest rates. Rises in rates can reduce the profits to shareholders while drops in interest rates can increase profits when it comes to Preferred Stock.

Because payouts are easier to access for Preferred Stockholders, there’s a greater deal of liquidity available to investors, and stock can be sold at any time without incurring a penalty.

15. Forex Portfolios

Forex Trading focuses on the purchase and sale of currencies in order to make profits. It goes without saying that these forms of investment are among the most volatile and risky that investors can undertake and it’s vital that if you’re planning to involve yourself in Forex Trading that you conduct plenty of research before diving in.

However, the heavy levels of volatility in Forex markets is the primary source of profit for investors. Here, there’s no limit on the currency that can be traded, but the use of brokers can be vital. The world of Forex Portfolios can be undermined by brokers who demand extortionate cuts in the returns you receive.

Be sure to perform due diligence when choosing a Forex broker to operate with, finding a strong broker with a solid CV can be the best way of ensuring that you can secure low-risk profits for your portfolio.

There are plenty of reputable Forex trading platforms in which you can build a portfolio, and places like eToro and Plus500 offer a good level of security in which to get started.

16. Cryptocurrency Trading

Firstly, let’s deal with the caveats. Cryptocurrency Trading is by far the most volatile way of making money from your investments. It’s also provided some resourceful investors with unimaginable levels of returns and thus deserves to be recognised as a proven way of investing money in the recent past – even if the future, as always, is entirely uncertain as far as the likes of Bitcoin, Ethereum and other key crypto players are concerned.

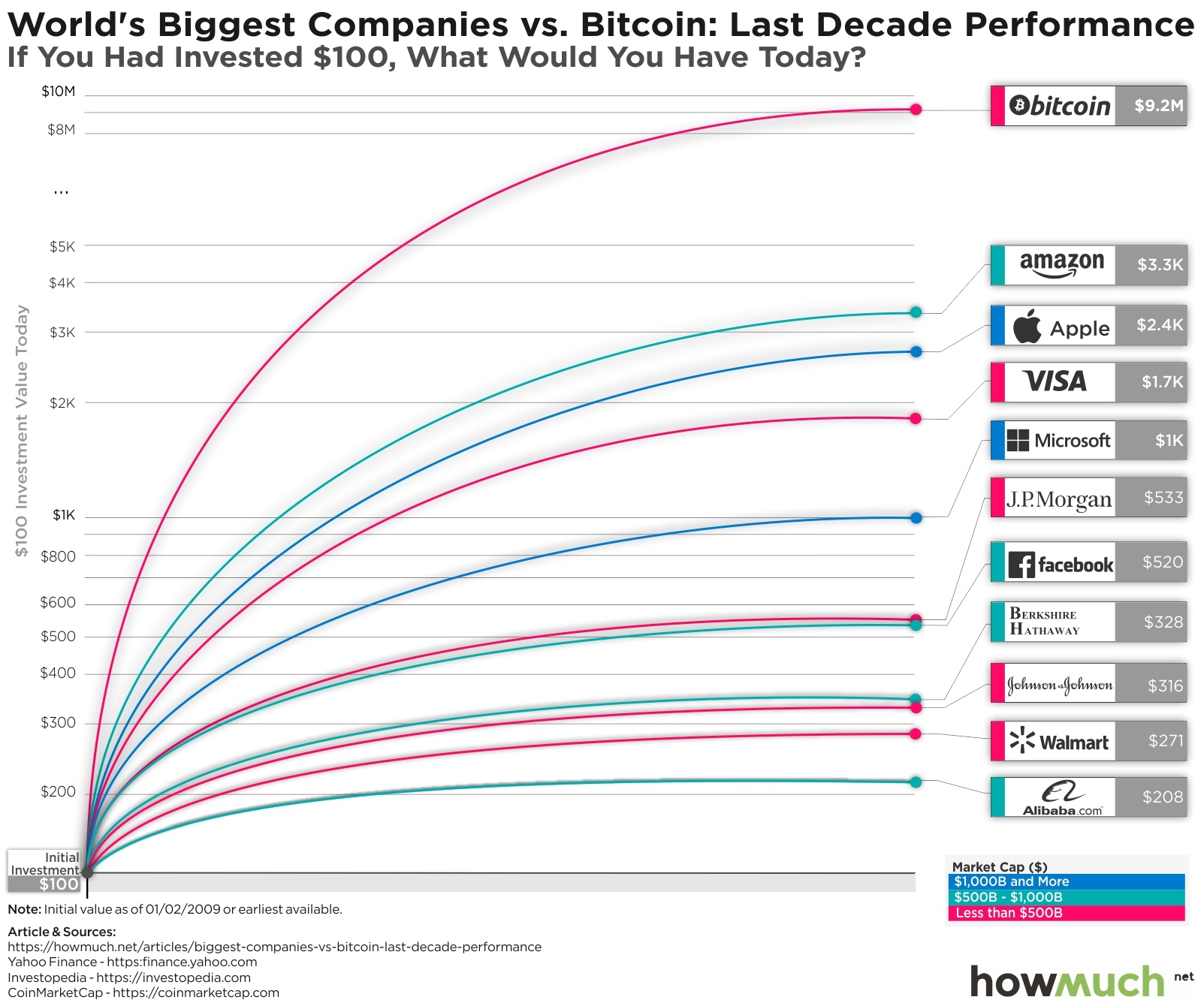

(Image: HowMuch)

As the somewhat crude graph published by HowMuch shows, over a period of 10 years, an early $100 USD investment in Bitcoin would’ve returned an astonishing $9.2 million.

However, it would’ve been virtually impossible to predict such a resounding success that digital currencies have managed to achieve in such a short space of time.

While there’s clear historical evidence of the cryptocurrency market increasing, there’s also evidence that could suggest that the market had already peaked in late 2017.

The world of cryptocurrencies are built almost entirely upon speculation, which makes them extremely difficult assets to predict. However, their intrinsic links to blockchain technology, and the continued interest that major companies, central banks and global governments have shown in developing their own successful cryptocurrency or stablecoin means that there could be plenty of logic behind the notion that the crypto bubble isn’t going to burst any time soon.

Fundamentally, many of the investment methods covered in this article will carry a significant level of risk, and while some will certainly help investors on their way to healthy levels of returns on their investments, it’s vital that you conduct your own research before creating a new investment.

In an economic environment that’s still braced for the full impact of the financial devastation caused by COVID-19, there can be a significant level of risk coming into the markets. So when it comes to lesser secure investments, be prepared for the possibility of losing out on your money.

Disclaimer: Any sort of trading involves risk. This is not an endorsement to trade or invest in any stocks.

![How Options Trading Works: The Ultimate Guide [2021]](https://daglar-cizmeci.com/wp-content/uploads/2020/12/Options-Trading-400x250.jpg)