Putting a value on a business is never a straightforward process, even for the most established of companies. When it comes to startups reporting little-to-no revenue with no tangible guarantees over the future, the task of pricing up an endeavour can feel virtually impossible.

For business owners who have a publicly listed organisation with healthy revenues and steady earnings, it’s worth valuing them as a multiple of their earnings before interest, taxes, depreciation and amortization (EBITDA), or by taking other industry-based multiples into account. However, it’s considerably difficult to put a price on a new business that isn’t publicly listed and may not start accepting custom for a matter of months and years.

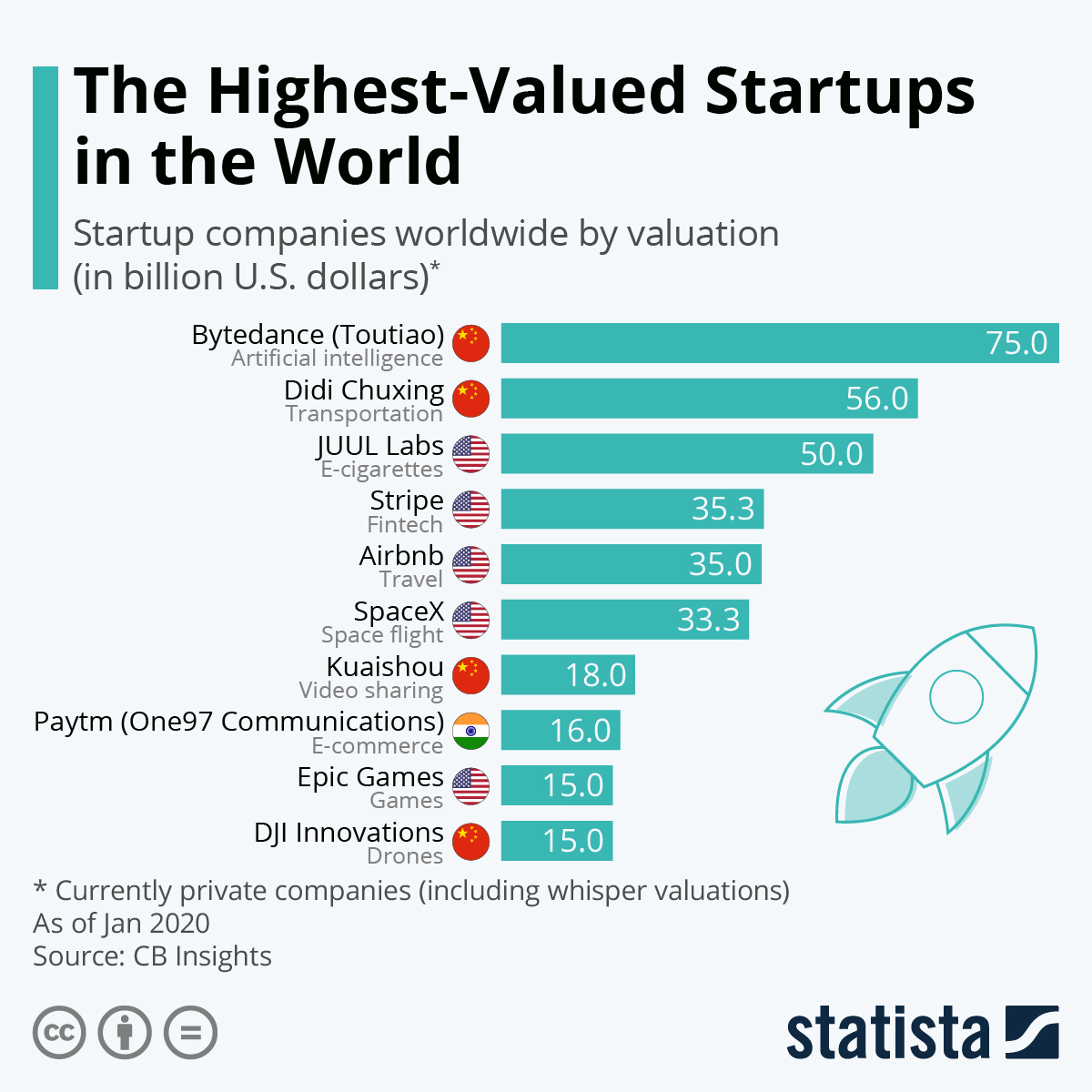

(Image showing highest-valued startups in the world. Image: Statista)

Attaching a value to your startup is a vital part of securing capital for your business. It’s also an important consideration to take before deciding to put money into one. However difficult it may be, accurate company valuation is essential in securing a startup’s future. With this in mind, let’s take a look at some of the most effective ways to accurately price up your startup:

Consider how much it would cost to do it all again

The Cost-to-Duplicate method of valuation focuses on business owners working out how much it would cost to recreate their company exactly the same as before from scratch. The notion behind this method is that an intelligent investor wouldn’t offer more money than it would cost to physically duplicate the endeavour. Entrepreneurs will typically need to take stock of their physical assets in order to work out fair market value.

In the case of SaaS businesses, for example, the Cost-to-Duplicate could be worked out as the overall cost of development time that’s gone into the creation of the software. For more tech-based startups, the Cost-to-Duplicate could refer more to the costs of the research and development undertaken as well as the costs associated with creating prototypes.

The Cost-to-Duplicate method of valuing startups is generally recognised as a strong way of figuring out a value for startups. This is because the approach maintains a level of objectivity due to tangible expense records.

It’s important to note the Cost-to-Duplicate valuation method has its own drawbacks. Most notably, the approach fails to take into account the future sales potential of a company along with its profit levels. Cost-to-Duplicate also struggles to take into account intangible assets, like brand recognition.

Because it’s a relatively unreliable way of formulating the true value of a startup and typically underestimates the price of a business, the Cost-to-Duplicate method tends to attribute the base price of a company. Fundamentally, the physical attributes of business may only amount to a fraction of its overall value from more intangible assets like staff knowledge and B2B affiliations.

Working With Market Multiples

Market multiples is a valuation method that’s typically favoured by venture capitalists. This is because it provides a clear indication of what the market rate for a given startup actually is. In a nutshell, the market multiples method determines a company’s value based on recent acquisitions of similarly sized companies in a relevant industry.

For instance, if you’re entering the market as a video conferencing platform, it’s possible to explore the acquisition prices of startups in similar industries to attain a rough market value of your endeavour. If a similar but more established firm sold for a specific price, it’s possible to break both of your companies down into their core properties and work backwards to find relative value. Fundamentally, if your business is a brand new startup, the market multiple involved would be lower – indicating that would-be investors would have a riskier prospect on their hands.

The issue with providing a valuation for a new firm is that its value hasn’t been realised yet. This means that investors will need access to comprehensive cash flow forecasts in order to gain insights into what an endeavour’s prospective earning will look like. If your startup is looking to take on venture capital investments, investors will likely only agree to place their trust in you when they’ve seen enough data to build their faith in your products and services. Where money is there to be invested prior to your startup generating an income, it’s important to have an appropriate valuation in order. After companies have scaled, it’s possible to generate valuations based heavily on earnings. While your startup isn’t earning, one of the most valuable methods of pricing your endeavour is based on market multiples.

Fundamentally, market multiples shine a light on the sort of prices investors are willing to pay to buy into your startup. However, the approach isn’t entirely flawless. All businesses carry a unique selling point, and as such, this makes it hard to find similar businesses. If your startup is nestled in an uncommon market niche, you may be hard pushed to find tangible examples. Many transactions can also be reported as undisclosed – leaving startup owners with much more guesswork to do.

Looking to Future Cash Flow

Startups that are yet to enter the market generally deal based on future expectations. This can be tricky for investors looking for clear evidence that their money is going to be well looked after in your company.

Luckily, discounted cash flow is on-hand to formulate a startup’s value based solely on their expected earnings. In a nutshell, discounted cash flow works by forecasting the level of cash flow the business will create in years to come and working out just how much said cash flow will be worth. This is done by calculating the rate of investment return for venture capitalists. Much like the case with market multiples, a tailor-suited discount rate is attached to startups due to the very real risk of the business failing.

Discounted cash flow is the most effective way of estimating a business’ value based on its future potential, but some investors are wary of this method due to the level of assumptions and conjecture involved in putting a price on a startup.

For a business that isn’t currently earning, discounted cash flow could be seen as nothing more tangible than a guessing game on the part of the business owner. Be sure to scrutinise your business accordingly when calculating a discounted cash flow model. Venture capital investors will be scrutinising data to find holes wherever they can. Be sure to avoid trying to overestimate your earnings.

Stage-Based Valuations

Primarily the domain of angel investors and venture capitalists alike, stage-based valuations focus on pricing up a startup by analysing its progression and development. Logically, a more developed startup will offer less risk for investors and carry a higher value.

Stage valuations typically take the form of ‘ballpark figure’ values attributed to early-stage startups based on the values that companies in similar industries attain at similar stages in their respective life cycles.

Such ranges can vary based on the startup in question and the investors involved. However, if your startup is looking for windfall from an investor, and you’ve only got a business plan to show them, you’ll likely receive low valuations. Whereas, if you’ve already demonstrated that you’re developing in line with your goals and attracting widespread interest, your business will invariably get assigned a higher value to reflect your progress.