The SME landscape is constantly transforming. In the wake of a post-Covid push for digitalisation, small business owners have begun to adopt a number of new technologies into their strategy, ranging from AI automation to fintech platforms, in a bid to streamline company growth.

As we step into a digitally dominated future, traditional business practices are quickly becoming redundant. One area in particular that has seen a significant transformation within the last decade is business financing. With a rise in multiple new startup funding methods, and a quick shift to fintech-based banking, traditional forms of money movement and company financing are starting to become irrelevant.

After a recent KPMG survey revealed that fintech investment has tripled since 2015, it’s time to explore the future of SME financing in a digital realm.

The question is, what does this mean for more traditional banking methods? As we discover the benefits of fintech adoption in the corporate industry, let’s delve deeper into the future of open banking, and the risks and rewards that come with it for SME owners in 2022.

Exploring The SME Playing Field In 2022

Before we jump into the future of small business banking, it’s important to explore the current trends and challenges the SME landscape is facing in 2022. From spikes in industry competition to the costs of inflation, there are a number of factors influencing the shift to digital financing post-pandemic.

A Spike In Competition

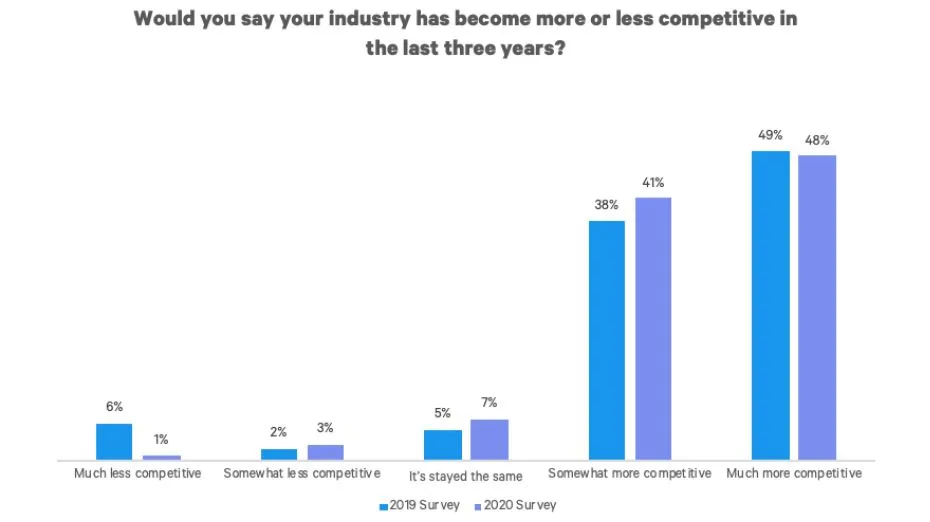

It’s no secret that the pandemic accelerated the shift online for a number of small businesses. As high streets dwindle and e-commerced boomed, the rise of the ‘online entrepreneur’ brought a new level of startup competition to the table.

In fact, 90% of respondents in a recent Small Biz trends survey claimed that their industry was now more competitive in the wake of the Covid-19 pandemic. While it is easier than ever before to embark on a startup venture, small business administration rates have risen under industry pressure.

After half of all SME leaders rated the e-commerce landscape ‘much more competitive’ in a 2020 survey, it’s no surprise that more than 20% of small business ventures are currently failing in their first year.

(Image Source: Small Biz Trends)

As SME leaders adapt to new levels of competition, a startup boom has only accelerated the adoption of new technology, digital marketing and digital financing. In order to address both consumer and competitor demands, automation has become the key to SME success.

Adopting Cloud Technologies

Cloud technology also continues to play a significant role in the SME landscape in 2022. With a market that is predicted to be worth $800 billion by 2025, cloud computing is dominating the corporate industry and streamlining data security and business financing.

Cloud technology improves data flexibility for SME owners, condensing big data into a cloud-based office that can fit into your pocket. Revolutionising remote working, the cloud has continued to reduce IT costs by removing the need for physical hardware and has provided more liquidity when moving money.

In fact, 70% of SMEs currently using the cloud plan to increase their investments in the evolving technology in the next decade.

Adopting cloud technology is the key to success, according to CEO of Berman Leadership Development, Bill Berman.

“Many small businesses do not have a strong digital presence. Success in the next ten years will be driven by your ability to use and leverage the digital and cloud technologies in use today, and your willingness to stay on top of whatever technologies your customers are using,” he claims.

Studies show that small businesses that have adopted the technology enjoy up to 120% more revenue and a further 106% more productivity, describing the digital shift as a game changer in the face of financing, cyber security and remote working.

The Impacts Of Inflation

Anxieties surrounding the rise of inflation across the globe continue to circulate across the SME landscape. In fact, 71% of SME leaders have deemed inflation their number one cause for concern in 2022.

After inflation peaked at 7.8% in April, SME running costs have soared. From supply chain disruptions to rising business expenditure, many small businesses are facing financial challenges as consumer demand surges.

This has not only affected how small business leaders manage their money but has significantly impacted venture funding. In an uncertain landscape, full of struggling startups, VC funders and investors are pulling back, raising both competition and the price of the funding rounds needed to qualify for investment.

Automated Financing

Widescale automation has revolutionised the SME landscape. From predictive data models to cybersecurity systems and automated credit control, the digitalisation of manual tasks is quickly changing the way we work and how the corporate sector operates.

Automated finance in particular continues to stand out in 2022. Playing a crucial role in moving an SME forward, automation of financial organisation ensures that money movement, investment decisions and business accounting are accurate, non-biased and error free, as human intervention is removed from the process.

With cash flow issues and poor investment choices ranked as the top two causes of small business failure, embracing fintech aids could be the key to success in 2022.

Addressing SME Banking Challenges

As the fintech market continues to expand at an exponential rate, a large number of SMEs are moving away from traditional banking. While they still account for 20% of all commercial banking revenues, small businesses are beginning to lean towards innovative online services and open, decentralised alternatives for their money management.

The question is why have traditional forms of banking become stagnant for SMEs? Let’s have a closer look at some of the key factors influencing the shift.

Poor Data Accessibility

When it comes to accessing SME-based data outside of a centralised institution, traditional banks struggle to assess an aggregated financial position in the same way as fintech platforms, that are able to use advanced analytic tools that can measure an SME’s total cash flow.

With a lack of data accessibility, traditional banks are unable to accurately rate an SME’s credit score and provide them with the same personalised service offered by open banking alternatives.

In addition to this, SMEs often find themselves limited in terms of funding and financing options when banking with a more traditional institution. Unlike most fintech-based platforms that can provide credit and service comparison within minutes, it is impossible to compare terms, services and rates amongst traditional competitors without supplying a full transaction history and a long list of financial data, making the process lengthy and potentially risky when inputting data into a number of systems.

Lengthy Service Times

Engaging with more traditional forms of commercial banking can often result in lengthy service times and complex customer journeys.

In fact, 83% of all European SMEs in a Fintechos study expressed that they wanted to be able to apply for banking products and services at a quicker rate, while less than a fifth of respondents claimed that they were satisfied with their banking experience.

As both front and back banking processes are often adapted to fit a retail-based audience, many SMEs struggle to receive a personalised service that speaks to their needs.

Lack Of Technological Advancement

In the wake of Covid-19’s push for widespread digitalisation, the lack of technological advancement within the banking sector has played a major role in an SME shift to open banking.

While host-host virtual connections are offered by some traditional banks to their consumers, they tend to only favour large corporates. Therefore SMEs are left to work through outdated portals, that are powered by manual uploads and a number of miscellaneous online steps.

In a centralised system, managing B2B payments is also an issue for SMEs. Without the ability to connect to a fintech-infused blockchain network, SMEs find themselves manually chasing overseas payments which can take up to five days to clear during a centralised verification process. With a lack of transparency concerning cross-border transactions, SMEs opting for a closed money transfer will often fall short in a new globally connected landscape, where demands are high and fast-paced.

A Fintech-Based Solution

Defined by Investopedia, “financial technology (Fintech) is used to describe new tech that seeks to improve and automate the delivery and use of financial services.”

The question is, could fintech be the solution to SME banking challenges? The financial services market has continually evolved in the wake of Covid-19, providing more digital payment methods than ever before.

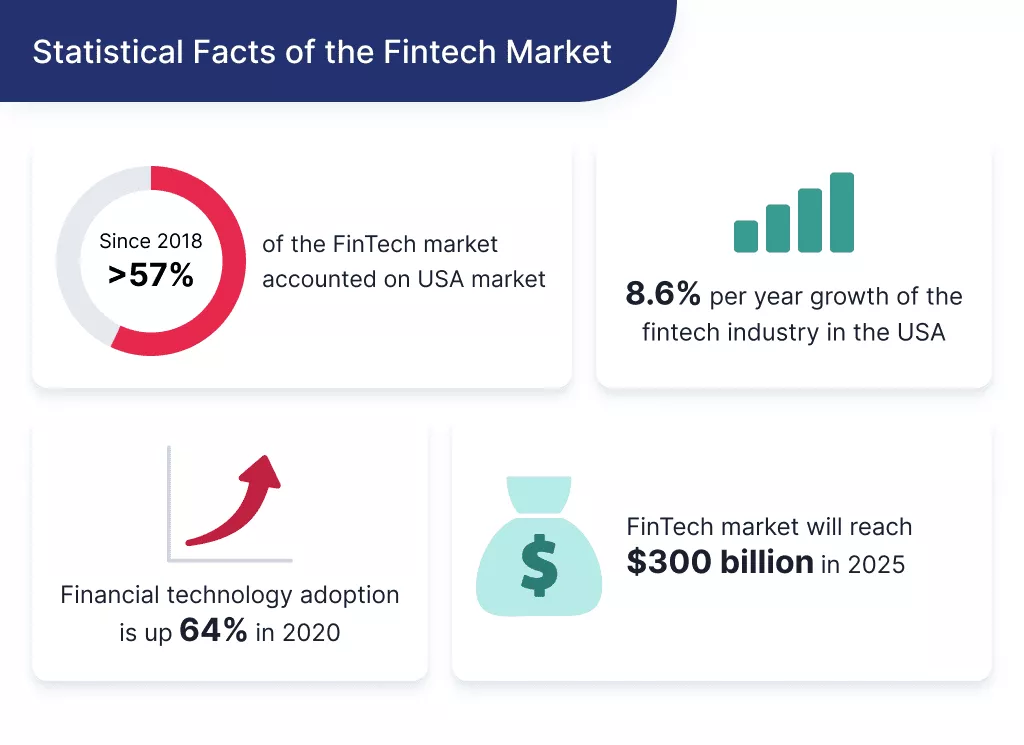

As new cryptocurrencies begin to dominate the consumer market, the future of finance is digital. In fact, an EY study revealed that 25% of SMEs have adopted fintech in the last five years, due to its varied functionality and ease of use.

(Image Source: SPD Load)

As you can see above, the fintech market is predicted to reach the $300 billion mark in 2025, with a large portion of funding originating from SME investment. In a globally connected B2B environment, small business leaders are quickly adopting fintech tech services to speed up and secure cross-border transfers, while also investing in predictive financing models, that can enhance smart market investments as the SME landscape expands.

“Fintech tools bring significant benefits for small and medium-sized companies,” claims CEO of Copenhagen Fintech, Thomas Krogh Jensen. “With a history of being underserved with financial services, SMEs represent low-hanging fruits that are key targets for a large segment of fintech solutions.”

Let’s have a closer look at some of the key uses of financial technology that are expected to trend across the SME landscape in 2022.

How Are SMEs Using Fintech Post-Pandemic?

Financial technology can be integrated into a small business strategy in a number of ways. From smart accounting to improving digital lending, SMEs are adopting fintech in order to streamline their financial growth and stay on top of competitors in an online global playing field.

While the fintech market continues to innovate a number of business practices, here are the most common uses of the technology in the corporate sector.

Enabling Borderless Transfers

While a cross-border transfer can take up to 5 days to clear in a centralised banking system, using a fintech-infused payment platform can deal with the same request in minutes.

On the back of a push for digitalisation in the e-commerce sector, a number of SMEs now regularly send money abroad in order to pay a global talent pool, overseas operation costs and supplier fees. As B2B relationships become a global affair, cross-border money movement has quickly begun to trend.

Fintech payment platforms such as Paypal, Wise and XE can operate in a wide number of currencies, while ensuring security, using a blockchain-based, decentralised system. Fintech integration ensures transparency for both parties involved in a capital transfer, making it a great option for SMEs that are planning to partner with global suppliers and industry competitors.

Improving Digital Lending

In 2017 alone, fintech innovation enabled SMEs to receive $6.5 billion worth of small business loans, that were unable to be accessed using a traditional bank loan-based route.

That number has significantly increased since, due to fintech systems pioneering to bridge the gap between banking and technological innovation. Eliminating long lists of documentation and the high turnaround time that comes with applying for an SME bank loan, financial technology can be used by business leaders to make the lending process much easier. Using a fintech platform, micro and small businesses that find it hard to qualify for a bank loan can apply for funding in seconds using an online system that is both speedy and convenient.

There is still a $5.2 trillion gap in funding for post-pandemic SMEs that fail to qualify for either VC/Angel investment or traditional small business loans. As fintech evolves, SME credit scores can be generated using AI-powered models that collate a wide range of financial data. This innovation will make more small businesses than ever before eligible for funding and help reduce the current funding gap.

Smart Accounting

Gone are the days of hiring accountants and tracking financial growth using a book-based system. Fintech evolution has enabled smart accounting apps to take the pressure off of SME leaders, in just a few clicks.

Using popular digital accounting aids such as Quickbooks and Sage Accounting, business owners can now keep track of taxes, expenses and payroll expenditures in a digital system. Not only does this save an SME time and money, these AI-powered systems can produce regular financial assessments and even influence future investment decisions based on historical payment history.

Could Open Banking Be The Key To SME Success?

As we move forward into a fintech-infused financial landscape, the term ‘open banking’ has begun to trend amongst SMEs. In a hybrid approach to financial management made up of centralised banking and third-party data sharing, both fintech and traditional banking processes are combining to improve SME financial services in a digital-first environment.

The question is, could open banking be the key to SME success or a risky financial move for small business leaders? Let’s find out.

What is Open Banking?

Defined by Chakray, “Open Banking is a mechanism in which customer banking information is shared to applications or APIs. In this way, an ecosystem is created that is conducive to generating business, solving needs, suggesting services and much more.”

Open banking is the key to financial personalisation. Relying on the data collected from previous payment histories, statements and credit scores, an open banking system can generate a service that fits the customer, while still operating within a secure, centralised banking institution.

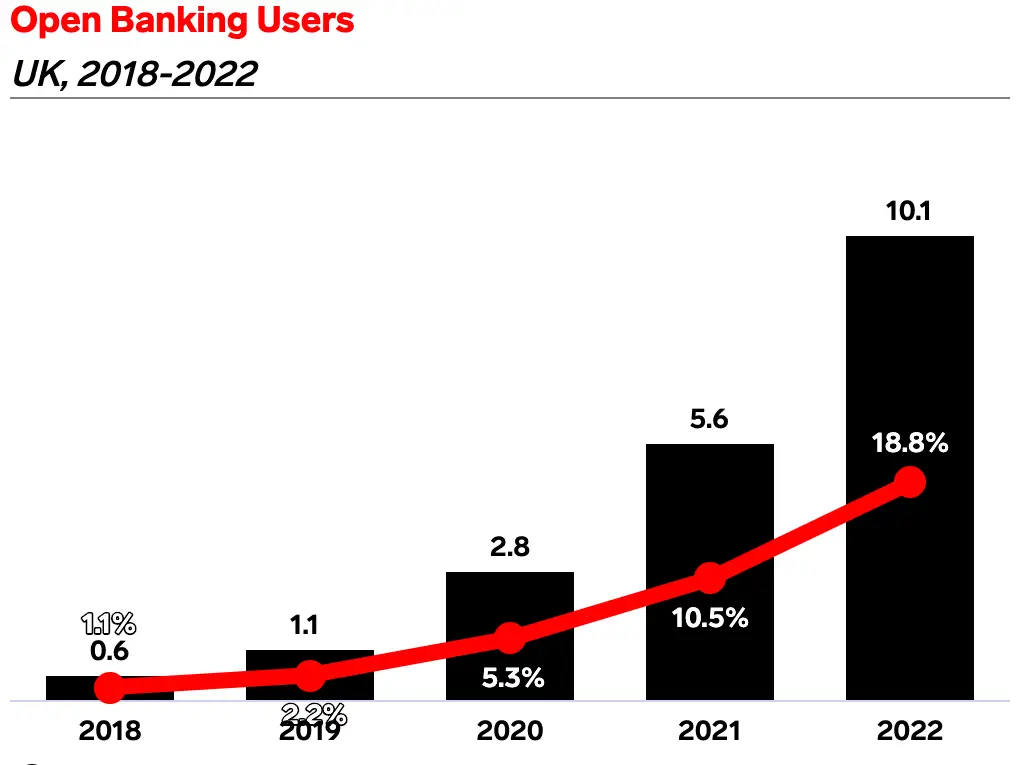

Today, just under three million online entrepreneurs use open banking to manage their finances and make the most of their money. The pandemic played a significant role in the shift to open banking after numbers jumped from one million consumers in January 2020 to double that just six months later. As SME numbers peaked, so did the adoption of digital finance solutions.

(Image Source: Business Insider)

With an 18% SME adoption rate in 2022, compared to 0.6% in just 2018, it’s no secret that open banking has seen significant growth since the onset of Covid-19’s push for digital banking.

The Competition and Markets Authority (CMA) believe that the adoption of open banking will eventually give SMEs greater control of their data in the banking industry. “Three years ago, we ordered banks to give people control of their own data to help transform the industry, driving innovation and stimulating rivalry,” Said a CMA spokesperson. “Today, more than two and a half million people are using open banking, with new customers coming on board every day. This is a remarkable achievement and still only the beginning of how far we can take this technology.”

Exploring The Risks and Rewards Of Open Banking

There are a number of risks and rewards associated with open banking. While raised levels of third-party data sharing can increase the risk of cybersecurity threats, over half of open banking consumers choose fintech innovation over privacy.

From improving personalisation to stepping up regulation, here are some of the advantages and disadvantages SMEs could face when introducing open banking to their financial strategy.

Advantages of Open Banking

A Personalised Service: Utilising the benefits of third-party data sharing, open banking uses predictive financial technology to index miscellaneous sources of financial data and manufacture a tailored service in response. By providing more sources of financial history, SMEs will receive an experience that matches their consumption logic and best fits their individual growth.

Data Transparency: Differing from traditional, closed banking formats, open banking prioritises transparency when handling customer data. In an open banking service, consumers have full control of their data and can choose who sees it and how it is used. In addition, fintech innovation has enabled SME leaders to access information at the click of a button and from the comfort of their smartphones,

Faster Funding: One of the key benefits associated with open banking is the ability to fast-track the financing process. With greater access to financial data comes greater access to a diverse range of business funding options. Using an open banking system, loan companies can provide credit offers quickly while also recommending services that are best fitted to the individual consumer’s financial situation.

Disadvantages of Open Banking

Teething Problems: While it may have taken off in a post-pandemic landscape, open banking is still a relatively new financial concept. APIs and third-party data collection have been around for the last decade, however, a hybrid centralised and fintech-infused system is still undergoing a number of teething problems in a financial playing field.

Cybersecurity Risks: While open banking initiatives ensure the security of data, 48% of consumers have cybersecurity concerns regarding the protection of their third-party data. As APIs continue to gain access to financial data, the risks of a data breach rise for the consumer. Engaging in open banking can leave SMEs open to fraudulent attacks, hackers and even insider threats.

Lack of Trust: While open banking is rated more efficient than traditional closed financial services, many consumers believe that a lack of interpersonal relationship between the bank and the customer makes it harder for business leaders to trust digital alternatives with large amounts of company data and capital.

What Does The Future Of SME Banking Look Like?

Despite the challenges ahead, open banking seems to be a trending financial strategy for a number of SMEs in 2022. In fact, researchers at PWC found that 71% of small and medium businesses in the United Kingdom alone were planning to adopt open banking before 2023.

The question is, what could this mean for traditional banking alternatives? As we step into a digitalised future of money movement, open banking is just another nail in the coffin of traditional centralised institutions, and just the start of a fintech focussed tomorrow.