Technological development has begun to blur the lines between traditional forms of banking and a digitalised future. As the financial industry continues to adopt emerging digital technologies to enhance the customer experience, it’s clear that traditional banking trends are embracing change in a post-pandemic landscape.

In fact, the financial industry is already evolving as investments in new technologies continue to hit record levels. As more banking giants adopt and invest in revolutionising fintechs, traditional banking is heading towards redundancy.

For the last decade, fintech competitors have been developing and delivering products that aim to simplify and personalise the banking experience. As consumers continue to diversify the financial institutions they associate themselves with, banking has truly become a digital affair that traditional protocols are struggling to keep up with.

As we delve into the future of fintech in a post-pandemic financial landscape, read on to find out the fate of traditional banking models and how technology may just be the key to a more efficient future.

Why Have Traditional Forms Of Banking Become Outdated?

It’s no secret that traditional banking formats are beginning to decline. Whether it’s a hybrid transition or a fully digital transformation, consumers are moving away from traditional banking processes as the population continues to move online.

In fact, a new study by Galileo found that while 77% of consumers still do their banking with traditional institutions, only half of them solely leave their funds in their physical accounts.

As digital payment apps such as Paypal continue to pave the way for fintech development within the industry, it’s clear that modern consumers are looking for an experience that mimics the blurred line between digital and reality.

“Consumers are looking for financial services experiences that meet them exactly where they are: on their devices, using various applications, accessing their money both traditionally and digitally, and doing more with their money,” states Seth McGuire, Chief Revenue Officer at Galileo.

“Across this industry, there is a massive opportunity to bridge the gap among all consumers and deliver highly valued engagements for those who use traditional banking and those who prefer digital.”

The question is, why have traditional forms of banking become so obsolete? Let’s have a closer look at the challenges of the traditional banking landscape.

Covid-19’s Digital Shift

Traditional banking has always primarily involved visiting your local institution to make and amend payments securely under one roof. However, in the wake of the 2020 lockdown, Covid-19’s digital shift has accelerated traditional banking’s demise.

Encouraging consumers to move online, the UK banking provider, TSB for example, saw a whopping 137% increase in online banking enrollment as a result of the 2020 pandemic.

In fact, as mobile banking continued to grow exponentially as a result of Covid-19, the number of physical branches shrunk significantly. As banking branches reduce hours and services, with some even encouraging consumers to move online, it’s clear that the digital shift has had an effect on traditional services.

However, this digital shift was coming into play way before Covid-19. Prior to the pandemic, the use of mobile wallets and app-based replicas of payment solutions accelerated by 36% with 1.6 billion users tipped to be using one form of fintech by 2023.

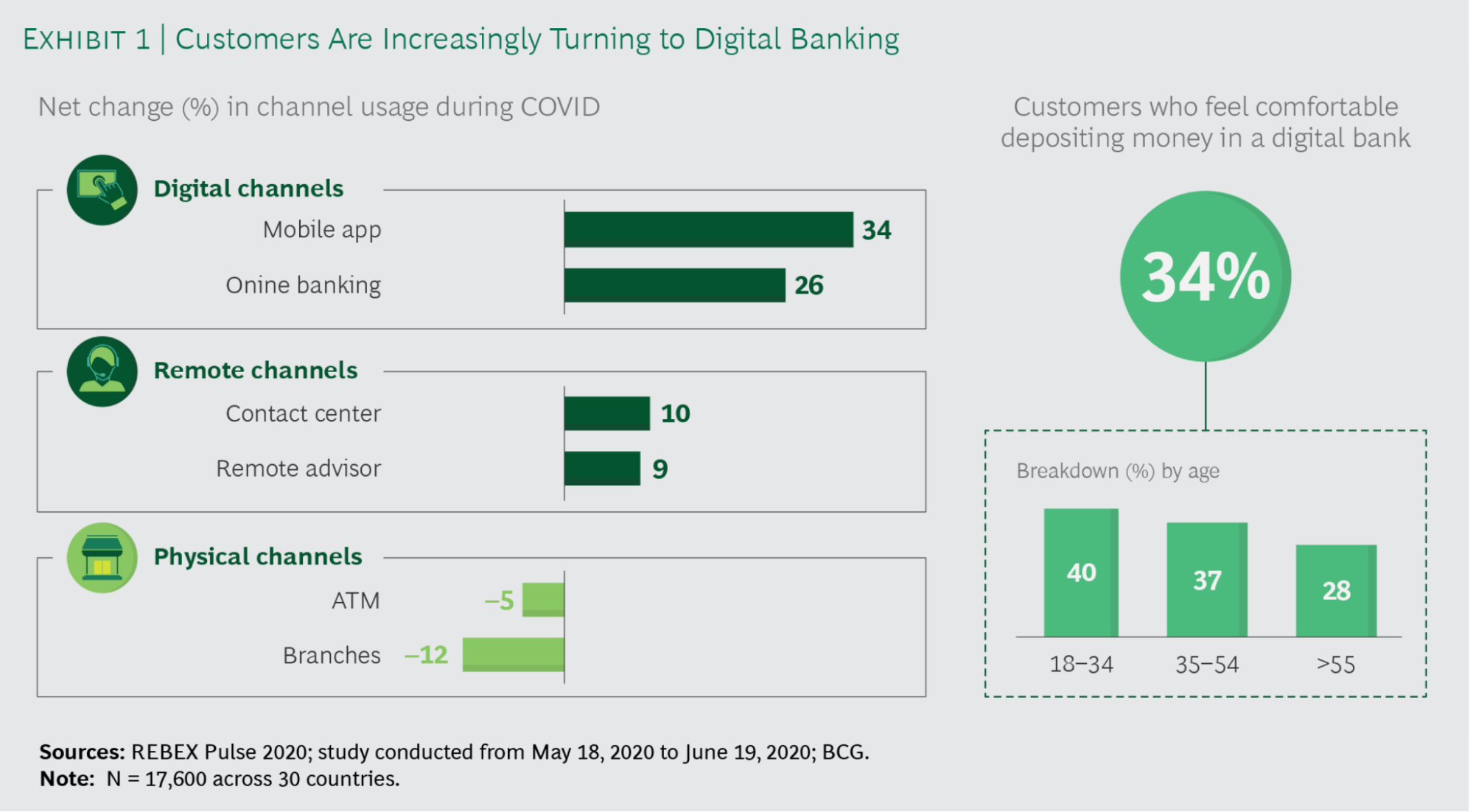

(Image Source: BCG)

As you can see here, 34% of customers already feel comfortable depositing money in a digital bank, and that number is expected to keep growing as more remote channels become available.

A Blockchain-Based Future

As traditional banks become obsolete in the face of the digital shift, let’s have a closer look at the prime technology that is facilitating the future of banking.

Blockchain is currently paving the way for fintech across the financial sector, decentralising payments and bringing cryptocurrency into the spotlight. With new digital currencies now being used amongst a global financial market, blockchain technology is leading a speedy and secure future of payments.

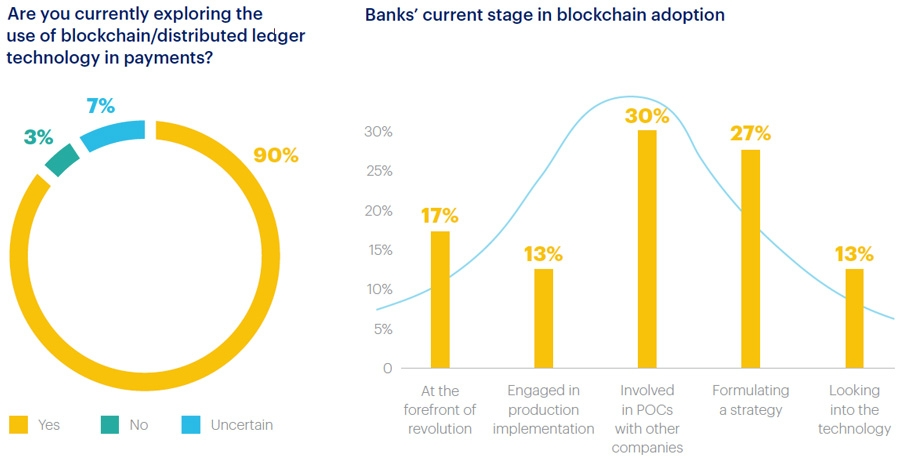

In fact, a 2018 Global Blockchain Survey revealed that 95% of 1000 of the world’s leading banking institutions were planning to invest in blockchain in the next ten years. Better still, a further 77% of fintech companies are already planning to adopt blockchain within their banking systems, further highlighting the crucial role it has begun to play in the industry.

(Image Source: Data Science Central)

As 27% of traditional banking institutions continue to formulate a strategy surrounding blockchain, here are some of the benefits of introducing blockchain technology to the financial landscape.

Improving Efficiency

It’s a well-known fact that blockchain technology is continuing to improve efficiency across the financial sector. From reducing swipe fees to cutting down the verification process, it’s no surprise that global money movers are encouraging its adoption within the banking industry.

In fact, blockchain technology reduces a standard banking remittance charge by 12%, making cross-border payments cheaper as well as speedy. Better still, facilitating money transfers using a decentralised ledger reduces verification time, making it easier to resolve a transaction.

Co-founder of Ethereum, Vitalik Buterin, states that blockchain adoption in the financial sector will continue to improve transparency and efficiency in a digital world.

“Blockchain is able to automate away the centre” he states. “Instead of putting the taxi driver out of a job, blockchain puts Uber out of a job and lets the taxi drivers work with the customer directly.”

Cyber Security

As Blockchain cuts out the middle man, consumers can also cut out the chance of their data being breached during the transaction process. With a high level of blockchain-based encryption, this cryptocurrency carrier enables new forms of transparency for banking giants, automating security checks for complete precision.

Using AI-generated profiling technology, consumers can be sure that their money is safe during cross border transactions. Blockchain continues to streamline complex workflows and enhance the remaining internal processes during a cross-border transaction. In return, the connection between critical infrastructures is digitally optimised, therefore eliminating large data exchange processes.

The Building Blocks Of Modern Finance

So what does the future of the financial sector look like? As fintech startups continue to multiply across the globe, the competition for customer retention within the banking industry has only grown in response.

As a result, a new era of collaboration is on the horizon for banking giants and fintech start-ups. On the back of blockchain’s success, the banking industry continues to adopt new forms of financial technology in order to stay in the race.

For example, banking giants, JP Morgan recently invested $25 million in fintech start-ups prior to the pandemic. Better still, Capital One has introduced fintech-infused banking cafes to their digital strategy in order to attract a younger, digital-savvy audience to their door.

Utilising automated software within the banking sector is no longer an option for the future, but rather a present-day reality post-pandemic. In order for traditional banking giants to stay in the game, the building blocks of modern finance are finally being recognised as key players in the industry.

The question is, what does the future hold for fintech’s success as a banking aid?

The Role Of A Fintech In The Banking Industry

In order to discuss the role that fintechs will play within the future of banking, we must first go back to its roots. Known as a combination of the words, financial and technology, a fintech can be described as a pioneering technology or software system that can improve the delivery of modern financial services.

Fintech first gained traction in the late 1990s when the internet began to emerge as a key player in modern society. Originally established to aid business owners and new entrepreneurs as they managed their business finances; its role within the banking industry is still relatively new.

Since embracing a new customer-centric focus, fintech is now used in a number of financial industries, ranging from retail banking, education and investments management, to fundraising and non-profit organisations. Spurred on by the adoption of cryptocurrencies such as bitcoin within the payments sector, fintech technology is can be used all across the globe to perform a number of a run of mill tasks. This includes moving money amongst accounts, facilitating crypto exchanges and depositing cheques.

In the case of banking, fintech software and even hardware such as virtual reality infused trading platforms are being used to enhance the customer experience. Revolutionising both back end processing and behind the scene monitoring, you’d be surprised at just how much of a key role fintechs play in the banking industry.

However, with only a 56% adoption rate amongst banking giants so far, there is still room for future growth within the industry.

The Benefits Of Embracing Fintech Within The Banking Industry

From securing transactions to joint investment, there are a number of benefits associated with embracing fintech development within the banking industry. Here are just a few reasons why fintech software could revolutionise the digital future of banking.

Secure Transactions

While traditional banking institutions may have their required customer information locked away in their database, they are still at risk of data breaches when moving money from one account to another, due to a long, centralised process.

When partnering with fintech startups, banking giants will reap the benefits of cutting edge technology paving the way towards a future of secure transactions. Enhancing the transaction authenticating authority using decentralised and AI-infused encryption, banks will be able to ensure each transaction is safe and secure.

A Huge Return On Investment

One thing we can ensure is a large return on investment for both banking institutions and partnering fintech companies as they continue to collaborate. As fintech adoption expands mobile banking functions, banks will see lower operating cost rates and a higher engagement rate from smartphone savvy consumers.

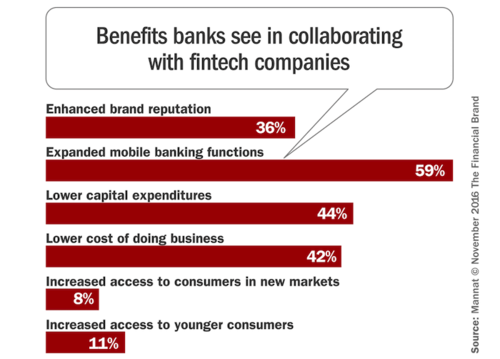

(Image Source: MSYS)

As you can see above, 44% of financial experts predict that banking giants will see lower capital expenditures in adopting fintech aids, and a further 42% predict that there will be a lower cost of doing business.

Joint Investments

Working together, the potential power of fintechs and banking giants combined could make room for new joint investment opportunities across the sector.

The partnership could open doors for investment in technology, innovation and a number of accelerator schemes focussing on different areas of banking, benefitting both parties and encouraging mutual growth in the digital landscape.

An Improved Customer Experience

Fintech’s role in facilitating online banking has significantly improved customer experience. As online banking tech is able to quickly adapt to changing market conditions, fintech has enabled banking giants to keep up with both consumer and industry trends, putting them on top of their industry competitors.

In fact, fintech adoption can aid credit score checks, cardless EMI, personal and SMB loans and many more banking services, while personalising the experience for each individual customer. Customers are not only more likely to pay attention to personalised services, but AI-generated offers and discounts that are tailored to the customer’s current financial situation, has raked in some serious revenue for banking giants.

Are There Any Challenges?

While fintech continues to revolutionise the banking scene, it doesn’t come without its risks. Constantly developing, many fintech startups are still in their experimental stage and can pose as a risk to banking giants who are struggling to diversify their traditional methods.

Here are some of the main risks and challenges associated with adopting fintech within the banking industry:

Changing Operations

One of the biggest challenges banking institutions face when introducing new technology to their business process is the transition from their traditional legacy systems to a newly digitalised alternative.

However, there are several options that are available for banks who are thinking of braving the transition. The first solution centres around launching a front-end application service for current customers. While applications provide a UX friendly interface for their growing demographic, this quick fix can serve consumers while important back-end developments take place at a calculated pace. Better still, banking institutions can split their remaining team in order to dedicate one half of the workforce to maintain their traditional legacy systems while the other half work towards developing a fintech-infused alternative.

Cyber Security Risks

As we continue to digitalise our data, cyber security breaches have become all the more common. With digitally complex financial systems in place, banks can be vulnerable to attack, creating lasting damages for both the institution’s reputation and its customer’s trust.

However, the risk of a cyber security attack is still significantly low as fintech becomes a more widely adopted security solution. Biometric advancements and code–generated passwords have made the banking industry more secure than ever before. Prioritising the implementation of fintech security systems is pioneering the way for a cyber-attack free future.

Fintech Can’t Replace Traditional Banking

One of the challenges that have sparked debate amongst the banking industry is the role that fintech will play in the future of banking. While financial technology will continue to revolutionise digital payments systems, it’s unlikely that it will ever replace traditional banking.

A high number of consumers still put their trust in traditional banking institutions and believe that they will hold their money both safely and responsibly. In order for fintechs to rise up amongst the ranks, they will have to remain patient and build consumer trust over time.

The Future Of Fintech

So what does the future hold for fintech? We’ve evaluated the benefits and addressed the challenges, but what can banking giants expect from fintech trends in the next decade?

Currently, 77% of traditional financial institutions are aiming to increase their focus on fintech innovation across the next decade. In an effort to boost customer retention and compete against standalone start-ups the banking industry is set to transform under fintech’s new reign.

As new data from Fortunately predicts that just under half of the global population now exclusively use digital channels to access their capital, traditional banking systems need to keep evolving if they want to remain on top of digital trends.

Here are some of the future innovations we can expect from fintech’s growing industry and how they are set to transform the future of banking.

Customer Facing Applications

A new study from Mckinsey & Company recently predicted that artificial intelligence could generate an extra $1 trillion in additional profits for the banking industry each year. As banking giants strive to improve their customer experience and data privacy, AI-generated fintech is tipped to pave the way to success.

Machine learning is expected to become more prevalent in the future of finance, assisting complex financial networks and enhancing cybersecurity systems while using minimal data. One of the key roles AI will play in the future of data privacy is decentralising centralised data sets by improving encryption, zero-knowledge proofs, multi-party computing and customer-centric analytics.

Better still, artificial intelligence will penetrate a wide number of customer-facing operations across the sector too. Using AI-infused fintech development, banking institutions are able to create consumer tailored products that enhance a personalised experience. From chatbots and Robo-advisors to automated transactions and facial recognition, the customer’s digital experience is constantly evolving.

In fact, new data from PWC suggests that 75% of banks are currently investing in a more customer-focused business model where fintech lies at the centre of success. Tipped to provide a hefty ROI moving forward, the evolution of hyper-automated software in the banking sector has only just begun.

Cloud Technology

Cloud technology is also tipped to revolutionise the financial industry in the coming years. With an annual market growth rate of 16.3% CAGR, cloud computing is expected to be worth $947.3 billion by 2026.

Financial institutions currently rely on the cloud to provide flexible scalability as the industry adjusts to meet digital shifts in demand. Banking, in particular, will tap into the cloud’s potential moving forward, in order to enable machine-to-machine communication and improve big data services.

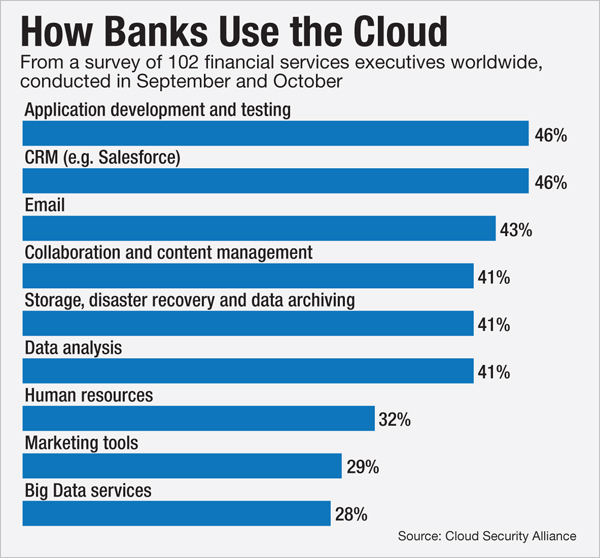

Scalability within application development and testing is predicted to increase the demand for cloud-focused elastic computing, enabling application models to scale both independently and efficiently as we see the effects of an architectural transformation. In fact, 46% of financial executives already use cloud-based systems when scaling application programming interfaces (API) and this number is only expected to grow.

(Image Source: American Banker)

Mike Beck, head of the threat analysis at DarkTrace states that cloud computing will also transform the future of cyber security in banking as critical data is stored on remote servers, rather than in the house.

“A lot of the changes we’re working on are taking the security that has been traditionally on-premises into the cloud, and using our technology there instead,” he said. “It doesn’t really matter where staff are located; the systems are up, they’re online, they have the full suite of toolsets available to them. Those who are going to struggle are those still dealing with legacy systems that are daisy-chained across geographical locations.”

Distributed Ledger Technology

Blockchain will also be a major player in the future of fintech. Distributed Ledger Technology (DLT) will continue to decentralise and simplify cross border transactions across the banking industry. Enabling the recording and synchronisation of data across a number of networks, DLT shortens the transaction chain and allows the storage of transactional data to be in multiple places at once.

In the case of fintech development, it will continue to underpin the financial landscape, as it assists the evolution of smart contacts, digital wallets and the rising popularity of NFTs.

The potential of decentralised finance also known as DeFi should also be noted as it continues to aid digital asset exchange. Using a form of smart contract, which aims to eliminate the need for a centralised intermediary, blockchain-based DeFi is tipped to broaden the access to digital assets such as NFTs and new forms of digital currency.

According to a 2021 Bank for International Settlements study, 60% of central banks revealed that they are either interested in or currently testing the potential of fintech-infused DLT. As new fintech start-ups on the market begin to partner with the power of blockchain, the sky is the limit for digitalised banking.

Looking Forward

Looking forward, it’s clear that we will see significant changes within the banking industry over the next decade. As fintech development booms across the financial sector, a large number of traditional banking institutions are worried about what the future holds.

In fact, 88% of mandatory financial institutions suspect that they will lose at least part of their business to start-up fintech competitors in the next 5 years.

As technological development evolves, the banking industry simply can’t sit this one out. Fintech will become the centre of their success as consumer demand for digitalisation grows and the players who fail to invest should be prepared to fall.