On the back of the highest global inflation rate recorded in the last decade, the startup funding landscape has reignited. As more business leaders turn to both dilutive and non-dilutive capital injections to stay afloat, turnover remains low while SME competition remains high.

A Business Impact of Covid-19 survey by ONS found that 45% of SMEs reported their profits have fallen by at least a fifth since 2020. Relying on backup funding to keep the venture alive, entrepreneurs are seeking external sources of investment in a competitive climate.

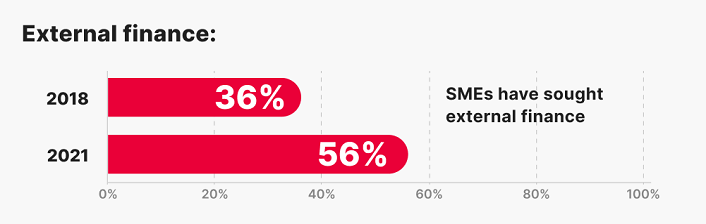

According to a British Bank Survey, over half of all SMEs have sought external funding since the onset of the Covid-19 pandemic.

(Image Source: British Bank)

This comes as over 12,000 companies file for insolvency in the first quarter of 2022, four times more than statistics from the same quarter in 2021.

In fact, one in three SME leaders are considering applying for at least one form of external finance in the next year, with government grants and SBA recovery loans remaining the popular capital source of choice for a number of small and medium enterprises. However, company owners must think smart when assessing their funding options in order to ensure they receive a capital accelerator that sits in line with their individual growth.

“The unstable economic climate in the UK and cloudy outlook means businesses will need to be careful when assessing their funding options,” claims Altenburg Advisory partner, Dan Barrett.

“Those looking to refinance their debt or acquire new funding will need to ensure they get the right advice and correct information on their options, so they can find a funding solution that best suits their needs,” Barrett comments.

Stick with us as we explore what the business funding landscape could look like in the second half of 2022, and reveal the pros and cons of the funding options available for SME leaders post-pandemic.

Exploring The Startup Funding Landscape In 2022

Ne startup funding trends continue to emerge in 2022. From a peak in non-dilutive equity funding to the impacts of a startup boom, a post-pandemic funding landscape is now rich with options for SME leaders at any seed stage or venture progression.

On the back of increasing startup competition, one in five businesses are expected to fail within the first year, according to the most recent statistics. A further 30% of all failures are directly attributed to cash flow challenges, rendering backup funding a must-have for SMEs as we move into an e-commerce-dominated future. As we navigate the funding options available for struggling startups in 2022, let’s have a closer look at some of the trends to look out for when applying for that all-important capital injection.

A Startup Boom

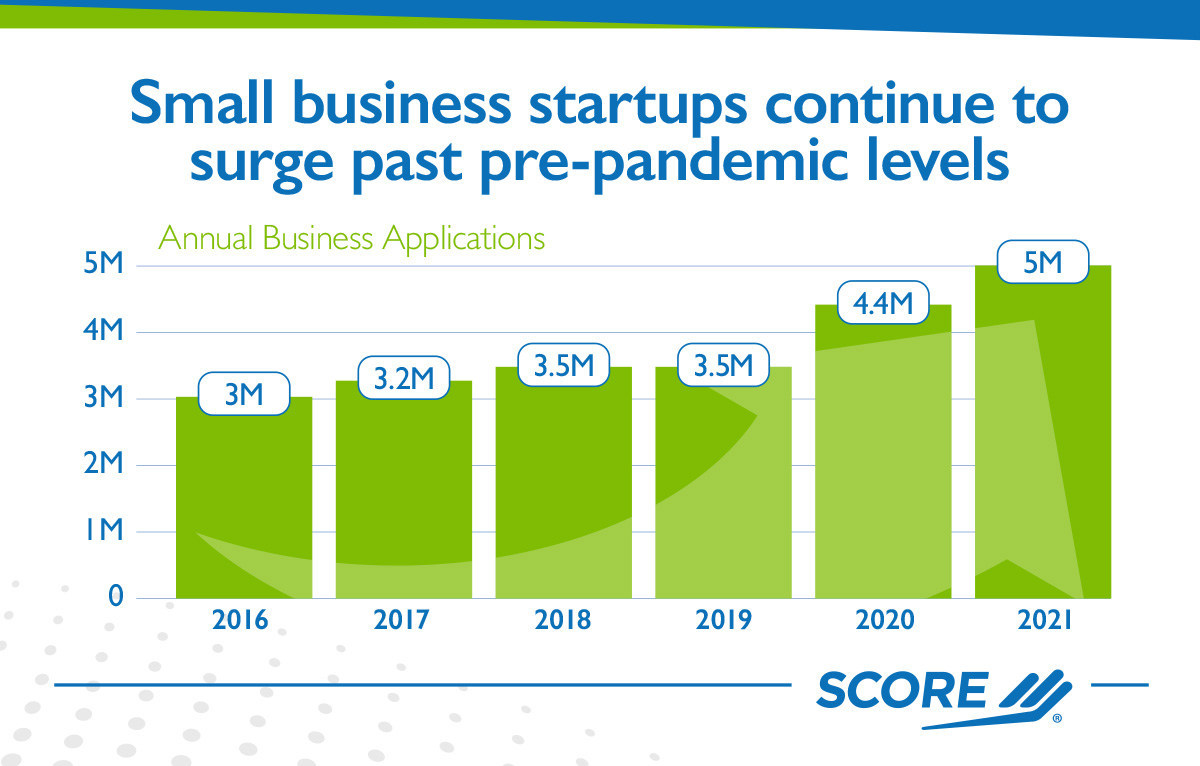

It’s no secret that startup applications have doubled since the onset of Covid-19’s digital shift. After 5.4 million entrepreneurs applied for a business status in 2021 alone, 2022 is set to see new application highs once again.

(Image Source: PR News Wire)

With a pandemic push for widespread digitalisation, starting your own venture has never been so easy. With a multitude of digital tools, AI-based automation and remote working aids at an online entrepreneur’s disposal and access to a gig economy full of freelance-based talents, it’s no surprise that a large number of corporate workers transformed their side hustle into their primary source of income in 2021.

However, while startup application rates multiply, challenges have also surfaced for online entrepreneurs striving to see a positive return on investment.

In fact, 43% of startup leaders now fear failure in the next 12 months as they battle through the impacts of inflation and a global pullback from VC and Angel investors. With less dilutive deals on the table, small business owners could be at risk as industry giants rival them in a race for consumer engagement.

The Cost of Inflation

As the corporate sector enters a period of post-pandemic recovery, climbing inflation rates pose great challenges to SMEs struggling to get back on their feet. In fact, 92% of small business owners surveyed by Business.Org claimed that their number one reason for requiring extra funding was to address a sharp increase in costs in 2022.

From increasing employee benefits to operations-based expenditures, a fifth of UK-based business leaders has seen their overall outgoings rising by 20% in the last 12 months.

“Since the pandemic began, businesses have been struggling to deal with the rising costs of inflation. Covid-19 just fast-tracked the inevitable—ongoing supply chain issues made it harder to access goods, which drove up the prices,” states Forbes Councils Member, Joe Camberato. “Businesses have two options in today’s business environment—stay lean and mean or commit to growth. At this point, it’s hard to manage anything in between these two choices.”

For those striving for expansion, applying for business funding has become essential for success. However, while some small business leaders are seeing their lowest turnover rate in five years, funding round expectations have only risen. As VC investors pull back and prioritise their existing ventures, fewer deals are being made in an unstable financial landscape.

With increased competition for dilutive funding on the horizon, inflation has only contributed to a dip in early-stage financing.

A Spike In Non-Dilutive Funding

While dilutive equity funding may have seen a sharp decline, non-dilutive debt-based funding models continue to trend in 2022.

In fact, a recent Lighter Capital financing report found that startups engaging in non-dilutive funding plans saw a $15k increase in monthly revenue alongside new gross margin levels of 50% or more.

From loans to grants to crowdfunding, protecting the direction of a venture has become just as important as financing for a large number of SMEs.

While equity investors are often the quickest route to a large capital injection, one of the key disadvantages of VC financing is providing the stakeholder with a seat on the board.

Entrepreneurs with a market-facing business strategy are quickly turning to non-dilutive funding sources in a competitive arena. In Europe alone, debt-based funding has peaked in the last six months, rivalling popular VC rounds.

Revenue-based financing (RBF) has taken a front seat especially, with a CAGR of 61.8% in Q1 of 2022. Rather than receiving a stake in the business, startups that apply for RBF funding give away a percentage of their gross revenue to the investor.

Benefitting both the startup and the investor, RBF supplements dilutive funding strategies. Not only can business leaders with a reduced cash flow delay funding rounds, but RBF can be used to protect equity during financial hardship.

Sustainable Credit Scoring

With the wide majority of leading industries now working towards a global net zero by 2050, sustainable investing trends have also had an impact on small business funding.

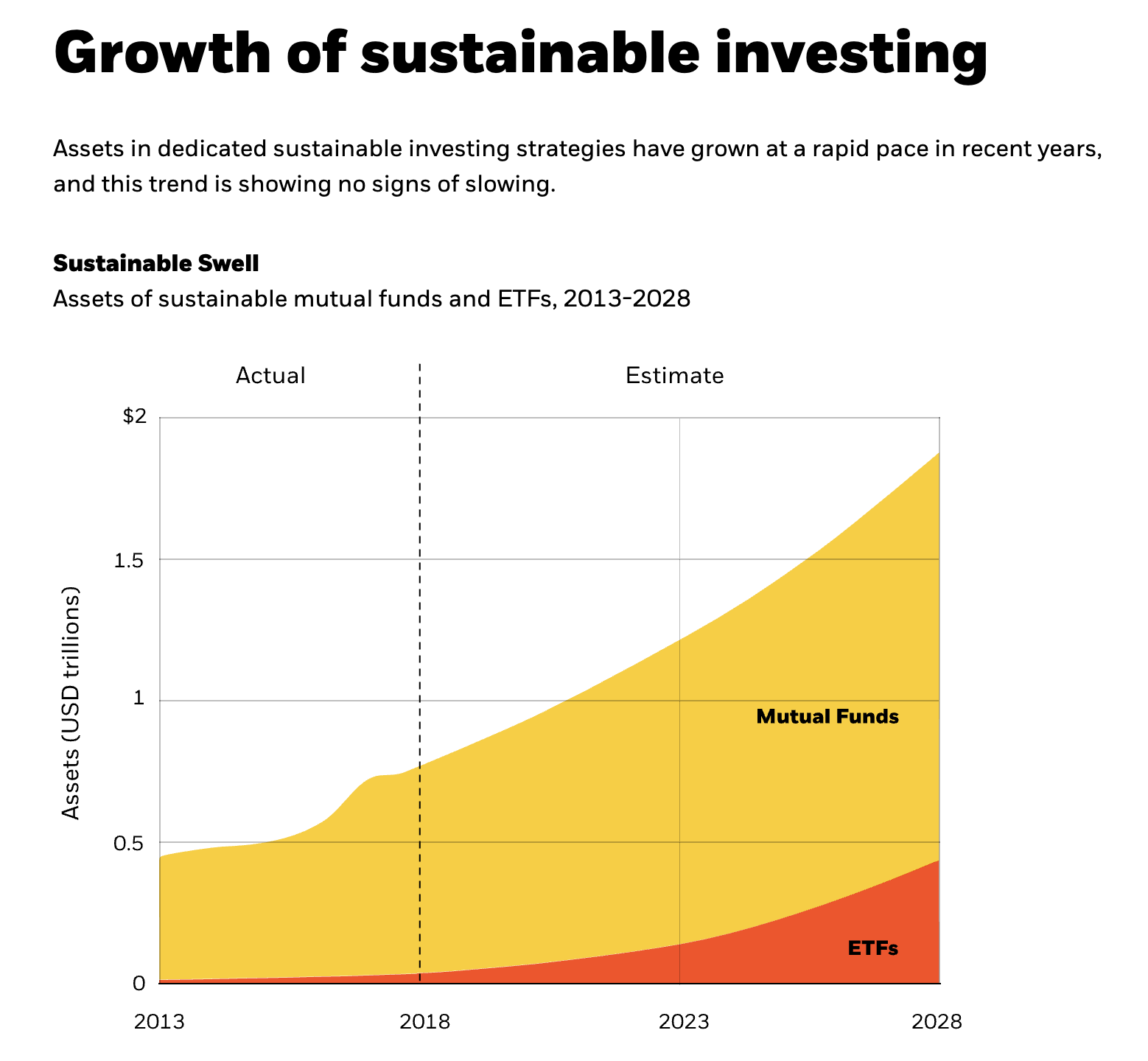

ESG investing took off in 2021. After a 60% increase in green VC investing, assets in dedicated sustainable initiatives show no signs of slowing in 2022.

In fact, in just the first half of 2022 alone, Cruchbase statistics have found that late-stage funding has increased the most, doubling in just a two-year time frame, with seed funding just on the tail at 40%.

(Image Source: Black Rock)

If anything, green investing has only increased the adoption of sustainable practices within the workplace. From cleantech innovation to sustainable packaging, the business visions of tomorrow will incorporate at least one form of carbon offsetting if they want to be prime candidates for dilutive funding.

However, while sustainable investing is at an all-time high, 48% of SMEs have stated their reluctance to take environmental action is directly attributed to a lack of business funding.

In response, popular risk consultancy firm 4Most, in partnership with cleantech leader Meckon, developed the ‘green credit scoring’ initiative in June 2022, in order to boost funding for carbon-neutral startups. In an attempt to improve sustainable practices within the SME landscape, 4Most is encouraging small business owners to go green in return for a capital injection.

“This project will build a virtuous circle of measuring carbon footprints, providing risk-based funding and boosting climate action,” claims 4Most’s client partner, Ivelina Nilsson. “To develop the Green Credit Score, we plan to gather data from potential borrowers to estimate the various aspects of climate change risk that they are exposed to.”

Which Funding Option Is Best For You In 2022?

There are countless funding options available to SMEs in 2022. As the startup landscape continues to expand, so do the financing opportunities for small business owners looking to get off of the ground.

The question is, which funding option is best for you? While dilutive funding can often offer the quickest path to success, signing a private equity deal can lead to loss of control and a minority ownership status. However, while non-dilutive funding models may seem more appealing, you might not receive that all-important capital injection needed to keep your post-pandemic business afloat.

Read on as we divulge our ultimate funding guide in 2022, and find a financing option that is right for you.

Venture Capitalists & Angel Investors

Known as the crème de la crème of the funding landscape, venture capital investment is one of the most well-known forms of dilutive financing. As a form of private equity, venture capital is awarded to startups with long-term growth potential, in return for a stake in the company’s future.

Typically coming from serial investors or Angel entrepreneurs, with a wide portfolio of business ventures, and a significant amount of experience in the field, the average initial seed investment stands at $1-2 million, while the average series A funding round equates to $14-15 million, according to Crunchbase.

While those figures may seem appealing, startups must demonstrate that they have a strong market potential if they are to be considered for investment. Not only should they be generating $500k-$4M in revenue to qualify for series A funding, but they should have a plan to expand 3-5x in the next 24 months in their current position.

There are a number of benefits associated with engaging in private equity funding. Not only do startups receive a vast amount of capital and an abundance of additional resources, but a large majority of VC-backed companies attribute their success to the guidance given by their investor as a voice on the board.

However, with the average VC typically acquiring 25-50% of a company venture, there are some significant drawbacks to providing VC partners with a voice on the board. Not only can they change the direction of a vision, but startup leaders can quickly find themselves in a minority ownership position.

Small Business Loans

For startups looking to stay in control of their company vision, applying for a small business loan or government grant, is a great method of non-dilutive funding. Whether you’re looking for short-term relief or a long-term repayment, small business loans are relatively easy to secure and can be accessed within a number of banking institutions or through a private lender.

In an era of post-pandemic recovery, there is also a multitude of Covid-19-based business loans to choose from, for that all-important cash injection. In fact, in the UK alone, £330 billion has been invested into the Coronavirus Business Interruption Loan Scheme (CBILS).

SMEs with a turnover of £45 million or more could borrow up to £5 million if they have been affected by the repercussions of a post-pandemic corporate sector. With over 34,000 loans now approved, 54% of SME leaders applying have now been eligible for non-dilutive funding in the UK.

However, while this method of funding allows a startup leader to stay in control of their company’s direction, there is a strict eligibility criteria that must be met if an SME is to be approved for a sizable cash injection. For newer business ventures on the block without a significant financial history, it can be harder for institutionalised lenders to provide an accurate credit plan that reflects a company’s financial trajectory. Instead, small business leaders are often left with high-interest rates that render a number of funding options too pricey for startup entrepreneurs.

As we step into a digitalised future, open banking trends are quickly providing solutions for startups struggling to receive an accurate credit score. Using open APIs to gather extra data on the financial history of small business ventures, open banking creates a bridge between the bank and the consumer, allowing for more loan-based opportunities.

Incubators & Accelerators

For early seed stage startups, incubators and accelerators can be used to boost initial funding, for just a small share of the company.

Known for providing small-scale financial assistance, usually, under $100k, incubator programmes assist early-stage growth, by providing knowledge, training and connections to startup teams, for just a 5-10% share of the business.

Accelerator programmes are also similar; however, they are often founded on private funds and aim to provide assistance to startups at a later stage of the expansion process. While incubators work mainly with the founder’s strategy and general vision, accelerators, take a much more streamlined approach, focussing on particular teams and products for a more targeted form of assistance.

For startups with significant growth potential, accelerator and incubator programmes are a great place to start on the tracks to receiving a larger VC investment further down the line. Partnering with industry experts from the get-go is an easy way to boost a company’s reputation, and appear more desirable in the eyes of a VC or Angel investor.

Revenue Based Financing

Revenue-based financing is a perfect option for startups looking to complement their existing equity or debt-based funding. Allowing entrepreneurs to remain in control of their venture, revenue-based investors take the returns for their capital investment from the company revenue rather than holding a stake in the business. With no ownership dilution, RBF investors are more like silent partners, rather than a voice within the company.

Revenue-based financing is also much cheaper than equity funding, as return expectations tend to be lower. While VC and Angel investors expect a 10-20X return on investment, RBF investors simply collect a percentage of monthly revenue, which is adaptable depending on the success of the venture each month. For example, if you’re a seasonal business owner, low-profit turnovers during quieter patches are taken into consideration, and capital is paid back in a way that suits the business rather than the investor.

With a flexible repayment system at hand, both the company and investor connect over a pattern of shared growth. Allowing founders to grow at their own pace, RBF can give startups time to reach funding rounds, rendering new forms of private equity investment more attainable.

Better still, unlike venture capitalists who are looking to ‘exit’ from a business venture once their equity returns are high, RBF investors are often in it for the long run, supporting a business venture over a number of years. Since the initial capital investment is repaid over a longer timeframe, founders are able to nurture their companies for as long as they need to.

Crowdfunding

While it may be a relatively new form of business financing, a global digital shift has only accelerated the adoption of crowdfunding in the corporate landscape.

Business crowdfunding is a great way to raise capital, without seeking equity or paying back a debt. Using numerous platforms on both the internet and across social media, entrepreneurs can build a campaign for public funding, in order to get their venture off of the ground.

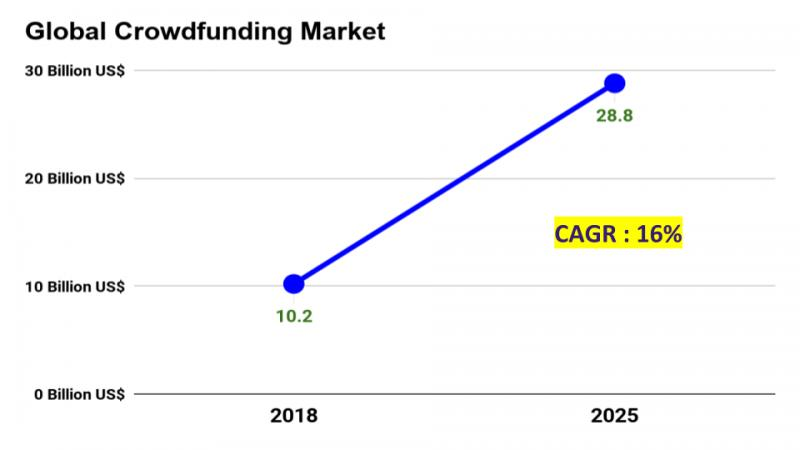

While success rates are still low, the average victorious campaign can rake in $30k-$1M, which is a huge financial boost for many struggling startups.

(Image Source: Open PR)

As you can see above, the crowdfunding market has grown exponentially on the back of Covid-19. As more online entrepreneurs dreamed about turning their side hustle into a full-time venture during a series of global lockdowns, many crowdfunding campaigns gained a global audience and social media virality in just a matter of days.

In fact, crowdfunding campaigns have been an asset to digital-based businesses looking to increase exposure. As audience-backed campaigns fell into the hands of a company’s desired demographic, many ventured gained both funding and a long line of new, attentive consumers, that continue to increase business revenue.

However, while crowdfunding success could be the answer to a startup’s financial wishes, only 39% of crowdfunding campaigns were deemed profitable in 2021, rendering it a risky financing solution for business leaders searching for true capital aid.

Friends & Family

Last but not least, it’s time to talk about the initial support system business leaders can turn to in their hour of need. While friends and family-based investments tend to be small and infrequent, little injections of capital can be what a startup needs to get off of the ground.

The average startup venture requires at least $25,000 in initial capital in order to have a shot at success in a competitive landscape. Whether this is spent on digital resources, a labour force or product production, most entrepreneurs need a significant amount of funding behind them before they even begin to search for additional funding opportunities.

This is where friends and family step in. Boosting a venture from within a close-knit circle can benefit both the startup and the members involved, as they may receive a cut from the profits if a venture takes off. However, mixing interpersonal relationships with a business venture can cause rifts, especially when capital is handed over unofficially.

What Does Tomorrow’s Financing Landscape Look Like

As we step into a new era of business funding, it seems as if both dilutive and non-dilutive financing methods will continue to prosper. As the corporate sector recovers from the impacts of both the pandemic and the exasperated pressures caused by inflation, startup leaders will have to lean on business financing to stay afloat.

While VC investors continue to pull back, equity-based funding is still tipped with the highest success rate in 2022. However, as open banking bridges the gap between startup financing and credit eligibility, post-covid digitalisation could see a positive future on the horizon for small business loan success.