At the heart of every successful startup is a great business idea. Some ideas can seem so simple that we wonder how nobody had thought about them before, while other ideas can seem so off-the-wall that we’re left wondering how anybody could possibly dream them up in the first place.

The fact that you’re reading this article now is simply down to a series of good ideas that would’ve seemed impossible to imagine let alone create just a couple of generations ago.

These innovative ideas don’t simply arrive in the heads of entrepreneurs as and when they’re required, and many of us who dream of coming up with the ‘next big thing’ often spend our time thinking about how best to approach the process of finding new ideas.

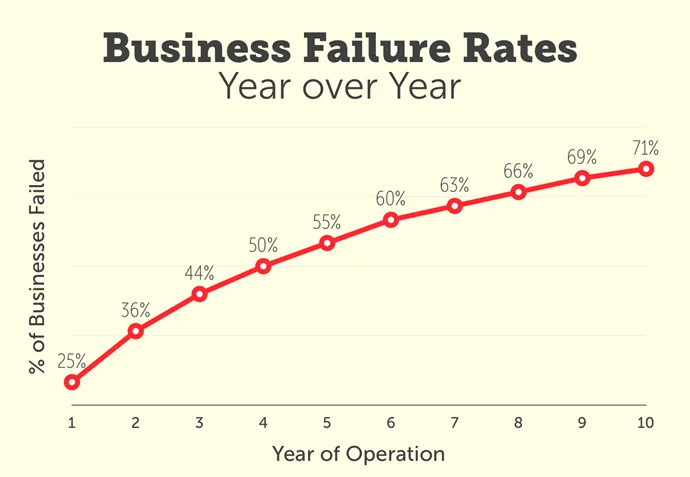

(Image: Neil Patel)

As we can see from the chart above, the vast majority of businesses struggle for survival over longer periods of time. The sad reality of business ownership is that all companies need to demonstrate strong fundamentals and promising operations long into the future to ensure long-term success.

With this in mind, it’s fair to say that a great idea alone won’t have the power to single-handedly drive a business towards prosperity over the course of 10 years, but it can certainly form a significant foundation.

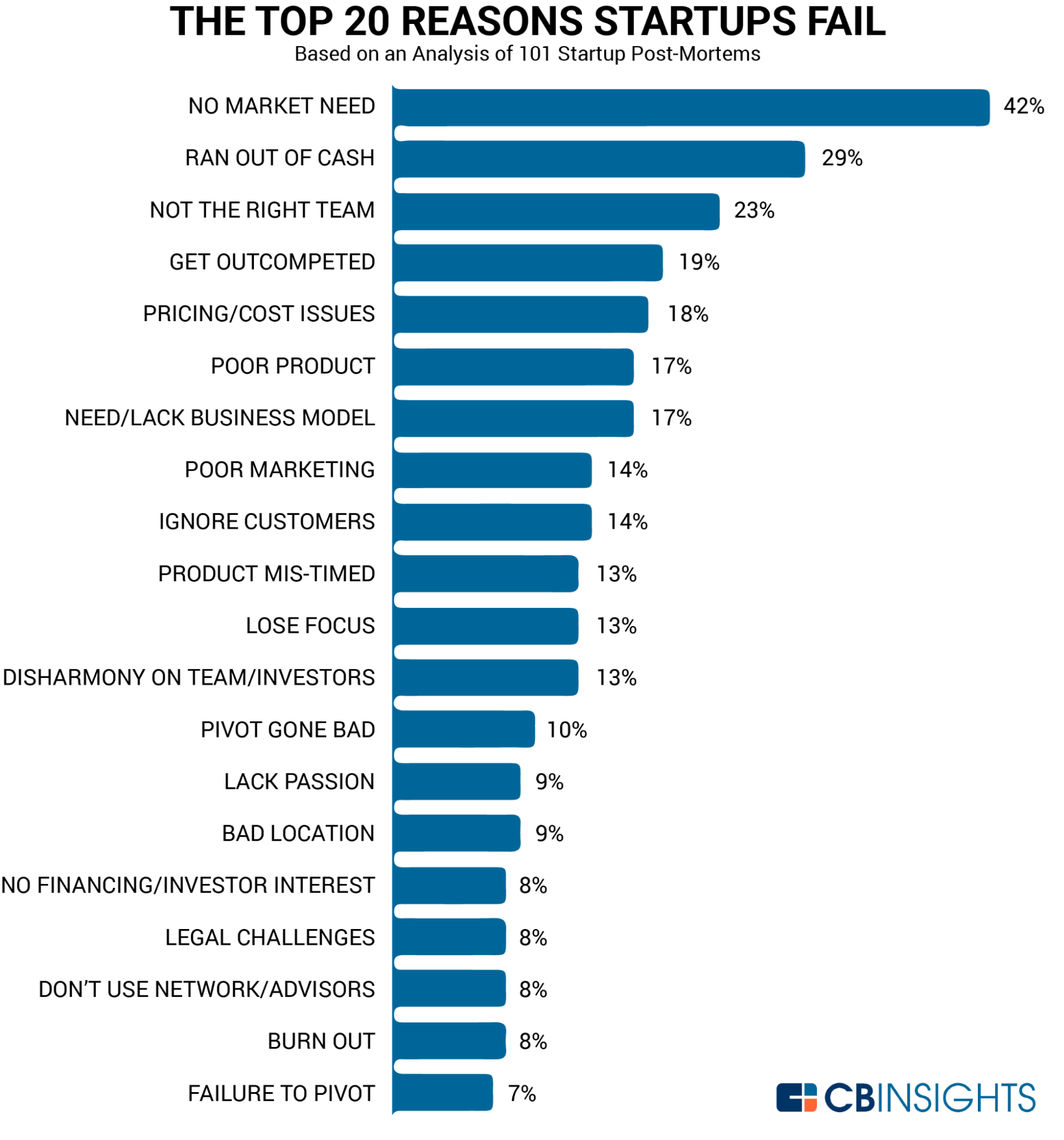

(Image: Entrepreneur)

Among the many reasons why businesses fail to take off, factors like a lack of money, failure to attain the right team, cost issues, insufficient marketing and a loss of passion can all come into the mix to undermine what may otherwise be a great idea.

However, we can also see that there being no market need for a product or service is by far the most common reason for failure at 42%. Other factors like competition, a poor product and a lack of a sufficient business model are among the key causes for failure – all of which can be remedied by having a truly innovative idea that resonates with customers.

But how can entrepreneurs come up with the innovative ideas that they use to send their businesses into the stratosphere? Is there a tried and tested approach towards finding the best ways to start a successful endeavour? Let’s take a deeper look at what it takes for entrepreneurs to come up with innovative ideas and explore some key examples:

Finding The Entrepreneurial Spirit

Before we look into how entrepreneurs come up with their innovative ideas, we should consider what sets them apart from other decision-makers in business.

There are some distinctions to be made between entrepreneurs and business founders or other risk-takers in business roles. While some within the industry may treat the terms as somewhat synonymous, there are key differences to consider in the characteristics that alter the way entrepreneurs should be considered.

One of the most important distinctions to be made involves the ‘entrepreneurial spirit’ and how vital it is when it comes to building and growing an enterprise regardless of who the actual founder of the business is.

What actually is the ‘entrepreneurial spirit’ however? The term can generally mean different things to different people – which may be expected in an entrepreneurial landscape that tends to revolve around the taking of risks, making subjective decisions and identifying opportunities where others can’t.

However, we can clarify what the entrepreneurial spirit actually is by looking at how successful entrepreneurs define it themselves.

Sara Sutton Fell, CEO and founder of FlexJobs, believes that the entrepreneurial spirit revolves around feeling empowered to take control of an endeavour: “To me, an entrepreneurial spirit is a way of approaching situations where you feel empowered, motivated, and capable of taking things into your own hands,” she said.

For Facebook founder, Mark Zuckerberg, entrepreneurial spirit is more about productivity: “The question I ask myself almost every day is, ‘Am I doing the most important thing I could be doing?’”

Both quotes focus on taking matters into your own hands and being as proactive as time allows. The entrepreneurial spirit is also largely about taking matters into your own hands and making vital decisions with confidence knowing that they could significantly impact your business.

It’s this level of bravery and boldness that entrepreneurs need to carry when it comes to dreaming up innovative ideas that may ultimately change the world and lead to the formation of the next big arrival on Wall Street.

With this in mind, let’s take a look at seven of the best ways in which those who encompass the entrepreneurial spirit can come up with the next big ideas in the world of business:

1. Seek to Solve Problems

The most simple way of coming up with a great business idea is to seek to solve the problems you already have. However, this solution is often easier said than done.

By looking to solve problems, you’re not being tasked with creating a new Google or Amazon, you’re simply innovating a solution that can benefit yourself or many more people.

One example of a company that was built to specifically solve the problems of many people can be found in Fresh Step, which was built to create a scoopable cat litter product that helps to dispose of the litter without owners needing to clean up and change the sand in a litter tray as frequently.

Ideas that have been constructed to solve specific problems are cropping up all the time. We can see new modifications being brought in to complement existing technology at a rapid rate. For instance, headphones are increasingly being developed with noise-cancelling technology. Smartphone apps like Waze have been developed to combine existing GPS and social media tech to help drivers to get from A to B faster and more efficiently.

In this regard, the vast majority of the products that we’ve become used to using were actually created as a means of solving a problem, including things like thermos flasks to keep food and drink warm, sunglasses to shield our eyes and fire extinguishers to keep us safe.

This approach to conceiving ideas requires you to train yourself to identify problems that are ripe for solving in an innovative manner. Once you’ve learned to channel your frustrations into a brand new idea, you’ll be able to set the foundations for a potential new company that’s bound to generate plenty of potential leads.

Take GoPro, for instance, the camera company that begun in 2002. Its founder, Nick Woodman, had just visited Indonesia on a surfing holiday and couldn’t find amateur photographers who had the necessary equipment to get good action shots of him surfing.

Off the back of this frustration, the GoPro camera was born – a wide-angle lens HD camera capable of capturing excellent quality action shots and video that other affordable cameras couldn’t compete with.

As you go about your daily life, whether you’re at home or work, try to train your mind to notice the things you find frustrating.

If you’ve been working in a certain industry for a while already, you may already have great insight into this matter, as there may be long-standing problems that companies have failed to effectively address over time.

Even if you’re currently working for someone else, try to use your experience to spot pain points in the processes you have. Once you get into the habit of spotting problems, it may even become an enjoyable pastime. After all, every problem you find is an opportunity to develop a new product or service – especially if it’s a shared problem among many people.

2. Find Inspiration From Around the World

As we’ve touched on in the point before, sometimes the best ideas you can get can be found whilst overseas. This helps to give you fresh perspectives on your markets back home and it helps you to discover new opportunities that may not yet exist in your local area.

For instance, Jimmy Cregan, founder of Jimmy’s Iced Coffee, came up with his business idea when he was travelling through Australia. He discovered that there was a large market for iced coffee there that didn’t exist back home and so created one himself.

Looking overseas for inspiration can be an excellent place to start, and you may discover a product that hasn’t yet been marketed closer to home.

In the case of Cregan, the Jimmy’s Iced Coffee founder believes that a business idea must be inspiring enough to occupy your thoughts at all times:

“If you like the idea of quitting your day job and becoming an entrepreneur, that’s great but you’ll need to find something you will spend more time on than anything else in your whole life, aside from breathing,” Cregan told The Guardian. “The idea needs to be embedded in your brain like some sort of bug that won’t go away. The idea won’t let you go to sleep, the idea will wake you up in the morning and it won’t leave your side.”

Cregan’s words regarding the obsessive nature of entrepreneurs points to why they’re regarded as a different breed in comparison to other prominent members of business. The startup grind is a process that many entrepreneurs can only endure if they’re truly in love with their idea.

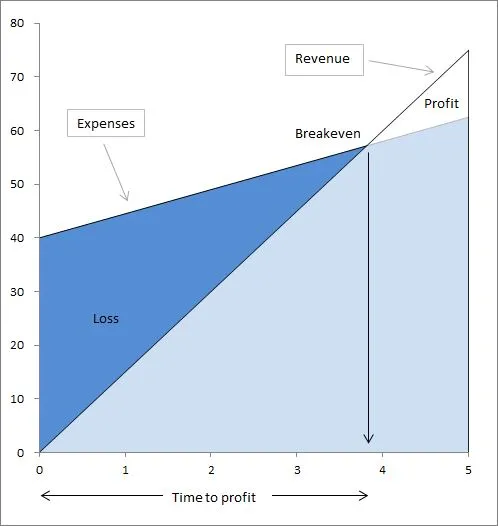

(Image: PlanProjection)

The diagram above illustrates the phases that businesses go through when attempting to become profitable. If an entrepreneur believes in their idea, they can push through the difficult days when their business is operating at a loss and reach a stage where they break even.

Up until that fateful point of profitability, it’s perseverance, money management, time, and passion for a good idea that will keep a startup afloat.

3. Find a Niche That’s Lacking Innovation

When coming up with ideas, it can be highly advantageous to look to markets that haven’t had many recent innovations. For instance, when Stephen Key realised that there were few new developments in the product information label markets, he decided to create Spinformation – a label consisting of two layers, a top layer that rotates with open panels through which users can see and a bottom label that can be read by spinning the top layer over it.

This innovation immediately found a market with companies looking to fit more information about certain medications designed for consumption. The extra space that Spinformation created on products meant that more detail can be included – enhancing the quality of service and information that users were able to access.

One of the key traits of a good entrepreneur can be found in their versatility, and it’s this ability that can help them to adapt better to niches and to understand if they’re ripe for some much-needed innovation.

Keep an eye out for traditional products and evidence of industries that have rarely evolved over the years. Is a lack of innovation down to highly functioning existing products and services? Or are there still pain points that can be ironed out with more modern approaches? The answer could pave the way for a money-spinning idea.

4. Plan Your Idea’s Evolution From Day One

When starting a business, it’s vital to develop an idea that has room to evolve as and when new needs emerge in the market.

For example, Jebbit, a technology company that originally offered a platform to pay students for the advertisements that they watched online, identified an emerging need for greater privacy and consent when it came to consumer data. The company adapted to create a platform for secure, declared customer data.

Technology is growing at a rapid rate, and there’s no guarantee that a good idea today won’t become outdated tomorrow, so it’s vital that you need to consider this when spotting your next big opportunity.

Harvard Business School Professor Clayton Christensen notes that technological innovations could either sustain innovation or disrupt them depending on how they specifically impact your business.

Let’s consider the path Netflix took as it emerged as a dominant platform for entertainment streaming services. The business actually began as a service that enabled people to watch movies without going to the video store and carried this out by posting DVDs to customers with prepaid return envelopes.

Later on, when streaming became more accessible for customers, Netflix adapted its offering to accommodate the new technology into its business model, and the company has continued to grow in this space ever since to become a market leader.

Despite streaming services being a considerable step away from Netflix’s initial business model, the company had to show the agility needed to adopt new technology to carry on serving its customers.

We only have to look at Blockbuster, Netflix’s more traditional early rival to see what happens when a good business idea fails to evolve as the technology around it develops.

When innovations emerge, you need to have a business idea that’s adaptable enough to evolve to continue serving its intended audience without being left behind by faster evolving competitors.

5. Find Inspiration From Social Sentiment

Failing to consult social media during the idea formation process means failing to tap into a rich array of conversations occurring among just about every target market imaginable all at the same time.

Social media users tend to be quick to spot and identify issues and problems that they’re having with their current products, services and processes in current markets. However, despite there being plenty of frustration with companies, very few consumers take matters into their own hands and come up with a functional solution.

Reading through the grievances that others are having with products means that you can attain a huge quality of insight into the problems that people are having across a wide range of industries that you may be able to solve.

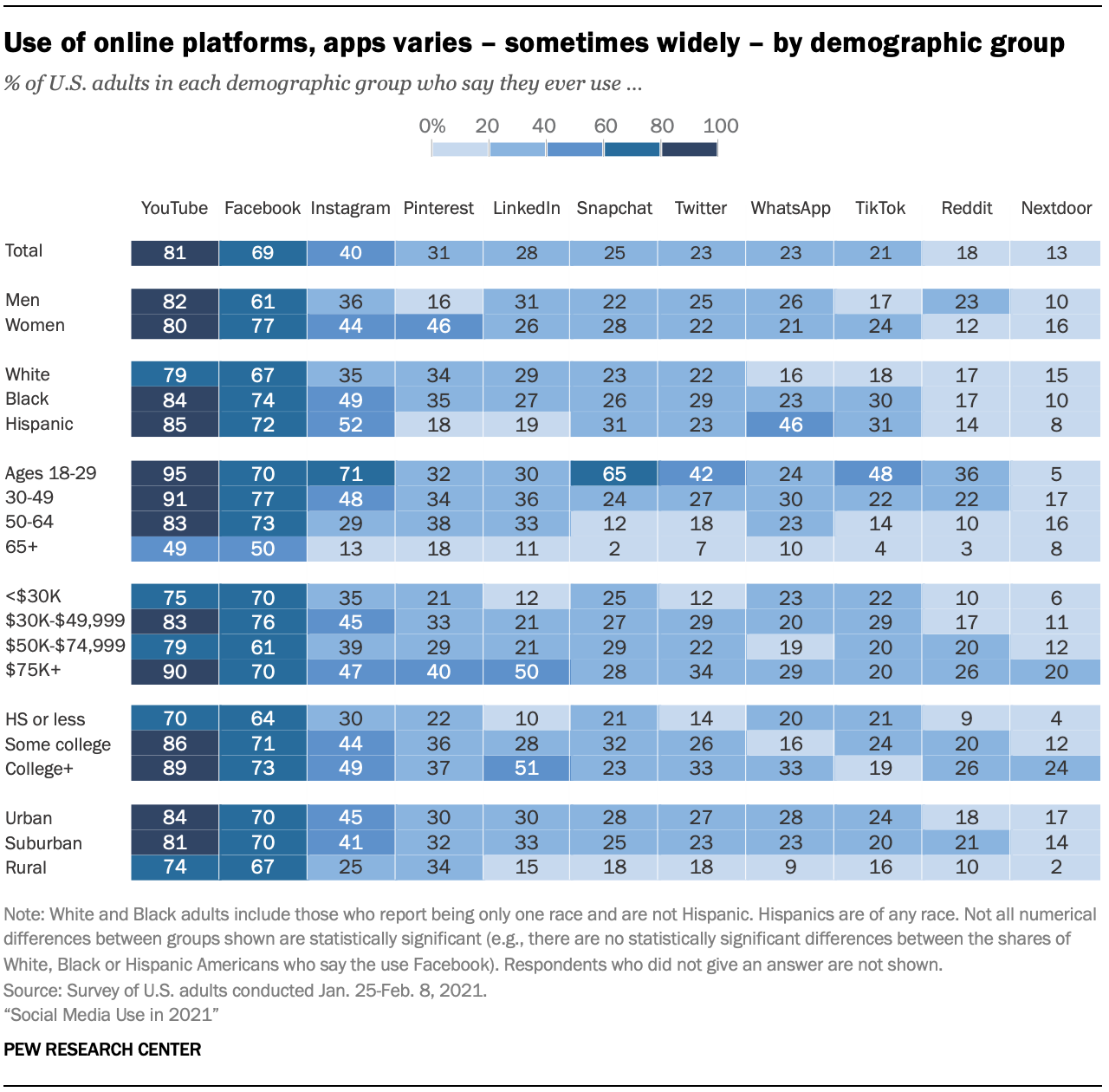

(Image: Pew Research Center)

As we can see from the richly detailed chart above, different social networks have wildly different audiences, and this is important for entrepreneurs to tap into when searching for – and refining – their ideas.

This means that the social sentiment you see regarding products on Facebook, which has an even spread of user demographics, may be different to the sentiment you see on TikTok, where the vast majority of users are under 49.

Social networks may also help you to identify more issues locally, meaning that you can set up your business to better suit the needs of the customers it’s likely to serve at the very beginning of its scaling process.

It’s also advantageous to consult online review sites across your chosen industries to keep on the lookout for common pain points and customer frustrations in existing products.

6. Work on Your Idea Before You Share it

It’s perfectly natural to want to share your idea with your peers, friends and family. You may feel the urge to share a good idea straight away to the people closest to you, but spilling the tea too early can lead to problems.

For instance, sharing ideas that lead to instant feedback may not always be as helpful as it might first seem – even if it comes from someone you love and trust. You could be excited about your idea only for it to be greeted with scepticism and doubt from your friends and family.

Although it may seem like a good time to get early feedback, you need to be mindful that you’re sharing your idea with many more people who won’t have studied the subject matter with as much intensity as you, and thus won’t be able to offer the level of insight that can really help to develop your idea while you’re still conceiving it.

Take the time to work and develop your idea into something truly consistent through the use of market research. Ask yourself all of the relevant questions regarding the time, money and resources that your idea needs and come face to face with the potential pitfalls you’ll need to navigate.

By conducting the due diligence yourself, you’ll have the answers you need when friends or family looking for holes in your plan. Furthermore, any negative feedback you may encounter is less likely to lead you to abandoning your whole project. Through better research, you can be more confident in the work you’ve already done on your idea.

Even if you’re not ready to share your idea with your friends and family right away, there are some people you should speak to early on. For instance, you should consider bringing in lawyers and manufacturers at an early stage, after all, you’ll need people on hand to defend your idea through intellectual property rights or getting a patent, and you’ll also need to create a working prototype early on as a means of helping you to secure funding.

7. Learn From People Who Think Differently to You

Nine days prior to the World Health Organisation making an official statement about Covid-19, BlueDot, a Toronto-based startup, had already alerted its clients about the spread of the virus.

The company’s AI technology, which is built on a big data-driven collection of health sources, moderated reports, news feeds, flight itineraries and masses of other data that’s been fine-tuned to identify an emerging crisis.

The technology was developed over the course of seven years. Its founder and CEO, Dr Kamran Khan worked to create a diverse team of over 50 experts to program the machine, from doctors, data scientists, geographers, veterinarians, software developers, epidemiologists and much more.

BlueDot’s algorithms are now called upon by various heads of state in order to track and contain the virus. According to Khan, the company wouldn’t be in the great authoritative position it’s in without the variety of input from its broad workforce.

“We had to learn to speak each other’s languages; understand each other’s perspectives,” explained Khan.

When developing your idea, remember to avoid falling into an echo-chamber situation where you’re surrounded by people who are similarly close to your perspective and maybe a little blinkered to potential challenges up ahead.

Once you’ve developed your idea, it’s worth opening it up to the scrutiny of those in the industry that you’re entering and those in other niches that your product may be impacting.

It’s vital to gauge as much opinion as possible in a bid to ensure that you leave no stone unturned in perfecting your idea. When we’re dealing with a vision that could lead to considerable business success, it’s vital to not only identify the perfect idea to fulfil your market needs but to conduct your due diligence before seeking to enter the market.

It’s through this blend of left-field thinking and in-depth research that you can foster an innovative idea that can secure the growth of your business.