The world of private banking is a rich and varied one that offers solutions for not only banking but investment needs and tax management to high net worth individuals (HNWIs). Unlike the commonplace presence of retail banking, private banking typically offers much more personalised financial services to clients via professionals who are dedicated to providing exponentially individualised wealth management.

Naturally, the financial security of HNWIs means that there are greater financial prospects in terms of investments that can be explored, such as hedge funds and real estate. Private banking offers greater levels of information and insight for clients regarding their investment options.

There are plenty of consumer banks that offer private services to aid HNWIs in growing their assets, and clients with larger accounts can expect to see appealing perks and individualised services – like instant access to the employees working on their accounts. In many cases, it’s also possible for them to contact the lead banker assigned to their account and complete significant transactions over the phone, rather than facing up to queuing in a bank.

But why is private banking so appealing for HNWIs? And what sets it apart from consumer banking and wealth management firms? Let’s take a deeper look into private banking and explore both its perks and drawbacks:

Private Banking, In a Nutshell

Private banking refers to financial services that are provided to HNWIs. These services don’t significantly differ from that of traditional consumer banks in terms of what they offer, but they bring a much more personalised approach to the fray.

Because of the amount of care that HNWIs require in looking after their finances, many consumer banks also offer more private services that provide levels of personal banking. The Bank of America, for instance, has a US Trust division set up to provide coverage for HNWI users.

Typically, private banking includes traditional services like checking and savings accounts, but it can also offer bespoke and specialised services too. For instance, Wells Fargo has its own ‘strategic borrowing’ function for users that are designed to help HNWIs make the most from their cash flow forecasts and tax efficiency.

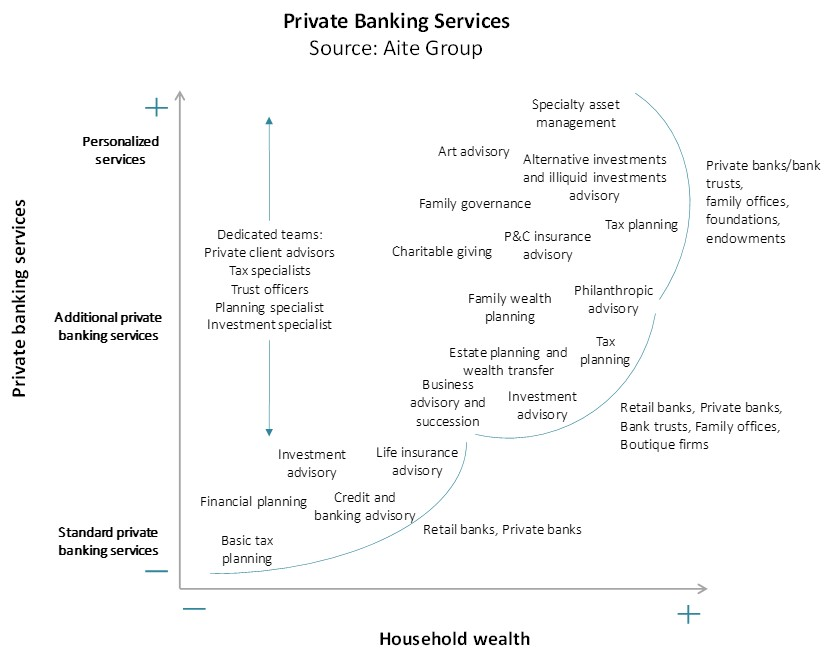

(Image: Aite Group)

As the chart above illustrates, there are plenty of personalised services available through private banking. Depending on the level of wealth held, more bespoke private services can be made available to clients.

In a nutshell, private banking helps HNWIs to utilise a fully customised financial strategy to manage their finances, investments and plenty more.

How Private Banking Works

Private banking champions the use of personalisation. This means that anybody looking to open a private account will likely receive their own ‘relationship manager’ or ‘private banker’, who’ll be assigned in order to oversee all matters related to their account. The private banker will perform complex tasks on behalf of their client – like arranging significant mortgages to setting up recurring payments for small utility bills.

However, the range of services offered by private banking extends way beyond the use of CDs and safe deposit boxes to manage a client’s wealth. Bespoke services can cover investment strategies, financial planning, portfolio management, personal financing delegation, retirement planning and wealth transfers.

While a client could be perfectly capable of accessing some form of private banking services with £50,000 or less in wealth, the majority of institutions typically insist on a benchmark figure of at least £100,000 worth of assets. The more exclusive financial institutions may insist on accepting clients with at least £1 million ready to invest only.

Private Banking vs Wealth Management

While there are certainly some similarities between private banking and wealth management, there are pivotal differences that are worth highlighting. Wealth management, for instance, involves charting a client’s aversion to risk and devising a plan that conforms to their financial targets. Private banking, however, provides more personalised financial and banking platforms to HNWIs. Private banks assign personal staff to their private banking divisions to handle the accounts of their clients.

Private banking varies from wealth management in the sense that this form of banking doesn’t necessarily require investing a client’s assets on their behalf. Private bankers essentially manage the client’s account – from cashing a cheque to transferring £100,000s between accounts. In many cases, they won’t look into facilitating an account’s growth through strategic investments – like in wealth management.

Although clients may receive advise on possible investment opportunities, private bankers usually don’t carry the authority to make or manage investments without permission from a client. Essentially, private bankers provide whatever wealth-related services that a client requires. Although this means that they would generally not be expected to take risks with their money, it’s possible for a client to grant permission for a private banker to make investments on their behalf.

Here, it’s possibly best to consider private bankers as personal financial assistants to HNWIs. They’ll handle and process large quantities of money, but they won’t be expected to have the freedom to make intuitive decisions based on the goal of growing wealth for a client.

Advantages of Private Banking

Private banking helps to bring clients a wide range of perks that are unavailable at consumer banking level. The level of personalisation offered helps HNWIs to dynamically manage their money in a fast-paced and highly digitised banking landscape.

In addition to this, there are also plenty of conveniently consolidated services available within an account.

Regarding the bank or brokerage, it’s also largely beneficial to add a client’s funds to their overall assets under management (AUM). Management fees and interest on loans underwritten can be fairly substantial for the private bank – however, with many institutions running discounted rates, there’s plenty of opportunity for prospective clients to take advantage of personal account management on their behalf for less.

Disadvantages of Private Banking

The level of exclusivity offered by private banking does come with some disadvantages. It’s worth noting that employee turnover rates within banks are typically high – even among elite private banking divisions. This can lead to some clients losing out on relationships built with their chosen institutions repeatedly through the lifetime of their account. There’s also the potential for conflicts of interest and loyalty issues. Here, the private banker is often compensated by their financial institution rather than the client themselves.

When it comes to investments, a client could be limited by the range of proprietary products offered by the bank. Furthermore, while the range of legal, tax and investments services offered by established private banks will likely be beneficial to the client, they may not be quite as creative as those offered by external professionals.

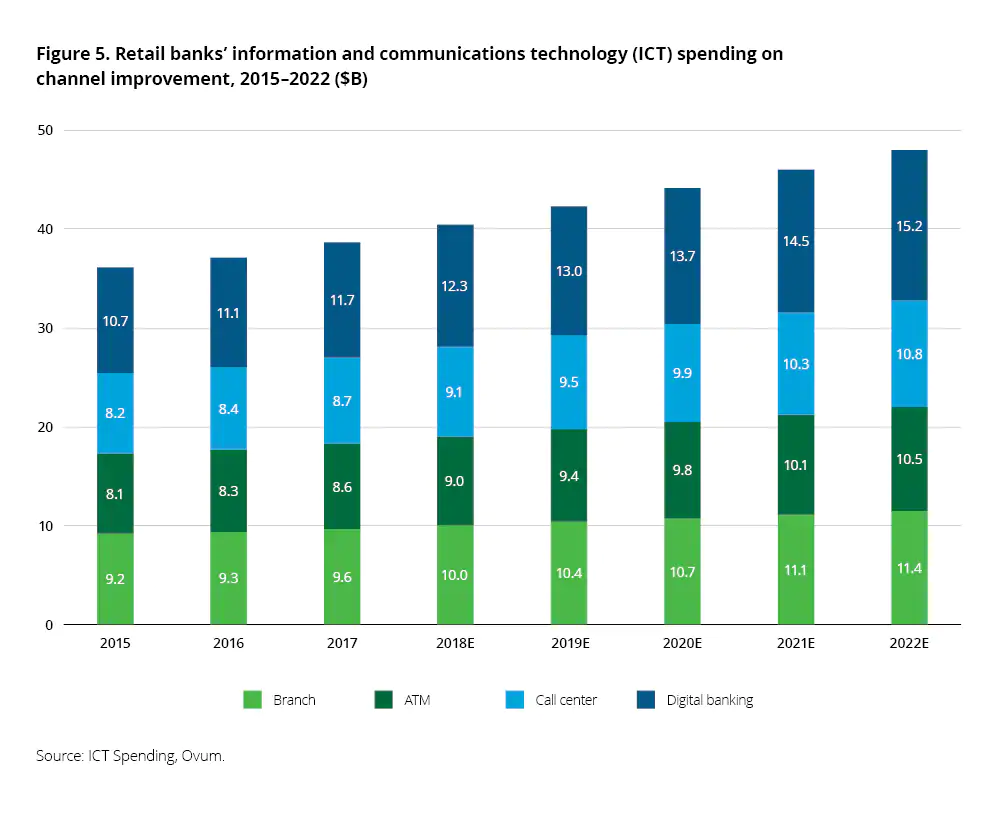

(Image: Deloitte)

It’s important to note that, while the fast-paced landscape of modern banking can be bewildering for HNWIs who already feel stretched by the demands of their careers, the technological capabilities of more traditional banking services are developing exponentially. As digital banking tools continue to progress, the gulf in convenience between private banking and consumer banking may drastically narrow.

Glancing at The Services Offered by Private Banking

The range of services offered for private account holders will undoubtedly vary from institution to institution, however, there are some recurring services that promise to bring significant levels of convenience to users:

Deposit accounts of HNWIs can benefit greatly from private banking – this is due to the preferential pricing that wealthy individuals may be in line to receive in comparison to standard account holders.

While it’s more readily associated with wealth management, investment planning can be a big part of private banking, and personal bankers can create customised investment strategies and portfolios to help clients to achieve their goals.

Real estate financing and advice can be capitalised upon by clients, with private banks capable of obtaining significant loans for primary or secondary homes.

As well as mortgage lending, private banks can provide specialised loans for HNWIs to help finance the purchase of, say, an aircraft, yacht or art. Furthermore, more flexible lines of credit can be secured through private banking.

Private bankers can also help clients with tax planning, due to a fluent understanding of existing laws and prospective legislative changes.

There’s also a degree of help available from private banks regarding estate planning. This helps clients to arrange for the seamless transfer of their wealth to future generations.

Managing wealth can be profoundly difficult for high net worth individuals who have to maintain a sharp focus on their careers as well as their finances. While wealth management can offer comprehensive planning and strategic investments, private banking helps clients to maintain a greater degree of control over their money. Investments can be made and profitable portfolios set up, but private bankers will seek to provide users with as much control as possible over the big decisions regarding their accounts.