For many entrepreneurs, the act of funding their startups can be an all-consuming worry. When you’re busy trying to bring a good idea to life, it’s vital that your mind is set on innovation and entering new markets. Fearful thoughts of startup funding can risk undermining your hard work entirely.

But the reason so many entrepreneurs spend their time worrying about finance is because it’s essential in launching startups. Ambitious small businesses rely on cash injections to survive and to purchase essential materials, office space, licenses and utilities to begin operating to the public.

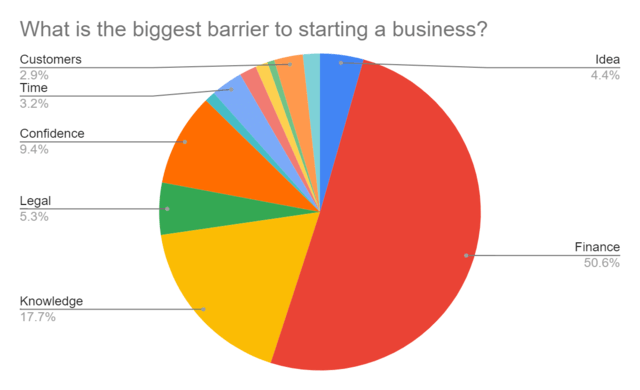

(Image: Startups.co.uk)

Finance is acknowledged as the largest barrier to starting a business by quite some margin. This guide has been designed to help startup owners to better understand their financing options. Below is a compilation of 10 different startup loan options. Each carries varying levels of risk and the amount of money each option generates can vary wildly too.

It’s important to note that there is no right or wrong option within this list, and some forms of loan can greatly benefit some startups while the very same choice could severely hinder the progress on another.

1. Family and Friends

The most simple form of startup loan that an entrepreneur can receive comes from the more bootstrapping approach of asking family and friends for help. Because this is a more informal way of generating early revenue, the repayment rates and equity that you can offer will be entirely up to you and your lender.

In many cases, it’s possible to borrow sums of money from friends and family without the necessity of adding interest to the sum.

Typically, borrowing from family and friends is an excellent and relatively risk-free way of funding your startup at its earliest stages. You can’t expect to raise the level of funding that a venture capital firm can bring in, but this shouldn’t matter, because during the early stages of your startup your mind should be set on developing your concept.

The amount of money you can raise from family and friends will depend on a range of variables – like the type of business you’re looking to start, their willingness to help, their belief in your idea, and the size of their personal wealth.

Borrowing from family and friends can be an easy process with flexible repayment structures. As long as you’re trusted, this can be a mutually beneficial investment between yourself and your lender.

However, the biggest drawback of borrowing from family and friends is the burden you can potentially put on your relationships. If things go wrong, not only you lose out but your loved ones do too. If you fail to explain to them the full risks involved with lending, then you could ultimately lose friends and anger family members who were simply trying to help.

2. Bank Loans

Traditional bank loans are a relatively safe way to gain funding for many small businesses and startups. While this approach to seeking short-term finance is one of the more popular out there, it’s important that you do your research before taking the plunge and signing up to a small business bank loan.

There are plenty of different types of loans accessible to you, with significantly varied interest rates and terms & conditions.

Securing bank loans isn’t straightforward, and you’ll need to mount a strong business case before securing your funding. It’s also essential that you have a good relationship with your bank to start with. If you’ve ever filed for bankruptcy or have accumulated a high level of debt in the past, this can all go against you when it comes to asking for money from institutions.

Some banks are willing to offer competitively low-interest rates, but it’s all highly dependent on your credit rating. However, if you secure a bank loan, you could receive a significant amount of money in order to take your endeavour to the next level – and you won’t even have to lose any equity for your business along the way.

However, the process of accessing funding in the form of a bank loan can be an arduous process due to the various rules, regulations and risk assessments involved. Some businesses can waste valuable time in attempting to secure a bank loan that never even becomes ratified. So if time isn’t on your side when it comes to getting a product to market, it may be best to explore your options.

3. P2P Loans

Peer-to-peer lending is a relatively new concept, but it’s steadily increasing in popularity as online lending platforms like Peerform, LendingClub and Upstart continue to grow.

(Image: Adroit)

P2P lending is a great way for borrowers to bypass the heavier rates and deeper regulations of banks and use the money of wealthy individuals to build their startups. This process can be fully automated within lending platforms and the lenders in question can receive automatic repayments on a monthly basis.

While P2P lending was originally identified as a form of lending for borrowers who would otherwise be rejected for bank loans, the growth of the service has meant that it’s a viable and social way of generating money for many entrepreneurs.

Platforms generally offer interest rates between the two parties involved in the loan, but lenders and borrowers can individually negotiate repayment rates and terms. Ultimately, this is a great way of gaining the money that you need without losing equity.

However, many P2P platforms carry steep punishments for late repayments and bounced returns, so remember to only take out a P2P loan if you’re confident that you can repay the figure, and its interest, back without delay.

4. Crowdfunding

Another fundraising process that’s growing in popularity is crowdfunding. With this option, it’s possible to raise the full amount of funding that you’re after online from the general public as the key stakeholders. Not too dissimilar to P2P lending, crowdfunding enables businesses to raise funds directly from people who have an interest in your endeavour.

Crowdfunders allow businesses to incentivise the money that people put into their fundraiser. Investors could either gain shares or equity in the company, or they could expect a product or service in return. Some businesses offer access to key figureheads or celebrity endorsers. In the case of authors fundraising their book, investors could be offered a credit on a page.

Crowdfunding is a great option if your business has plenty of growth potential that will attract widespread attention. However, the fundraising process could take weeks and months – with no guarantee that the idea will attract enough attention among potential investors.

The biggest positive is that you can use crowdfunding to better understand the scale of your idea. The faster you are to receive money, the more sure you can be that you’ll have a successful product. In turn, more investors mean greater revenue potential.

Perhaps the largest drawback of crowdfunding is the fact that many businesses will need to launch some form of a marketing campaign to alert potential investors to a product’s existence. When funds are already scarce, this can be highly problematic for a startup.

5. Venture Capital

Venture capital investors typically invest considerable sums of money in return for equity in a startup or small business. Usually, their objective is to accelerate the growth of the businesses in order to see a healthy return on their investment in a short time frame.

If you’re a startup that can show good growth potential, and, significantly, you’re happy to lose equity in return for investment, venture capital can be an excellent way of securing your future. After all, 70% of a successful small business is better than 100% of nothing.

(Image: Fundable)

Venture capital stands as one of the more commonplace funding sources when it comes to setting up a startup. Another appeal of this form of loan is that venture capitalists tend to offer a high quality of mentoring in order to help you to steer your ship towards success.

As well as funding and mentoring, venture capitalists can offer the businesses they help with strong industry contacts in order to help your progression.

Despite there being clear perks and potential for scaling, the biggest con associated with accessing venture capital comes from the fact that many entrepreneurs will be faced with giving up equity in their business in return for money. This may not seem like a big deal today, but if you give up a 30% chunk of your business and it eventually sells for £10,000,000 – you’ll lose £3 million on the deal.

6. Angel Investors

Angel investors are wealthy individuals who may be interested in providing funding in exchange for a share in your startup. Behaving in a not-too-dissimilar manner to venture capitalists, angel investors can operate in groups or they can behave entirely independently.

Utilising angel investors isn’t a great plan if you’re dead set on maintaining full control of your business without surrendering some equity. However, a clear positive associated with angel investors is that they’re often capable of providing invaluable insights to entrepreneurs as a means of getting their endeavour on track.

However, angel investors can also be difficult to find, and in virtually all cases, you will be required to lose equity in your business in return for funding.

7. Guaranteed Loans

Guaranteed loan initiatives such as the Enterprise Finance Guarantee are designed for small businesses that aren’t able to qualify for bank lending. The reasons for this could be that they’re unable to put up security or don’t yet have a trading history. If your startup falls into these categories, it’s important to be aware that you will still need to competently demonstrate some form of actionable business plan.

The perks of guaranteed loans are that they can offer businesses a lifeline where founders have exhausted all other routes and have found themselves continually turned down. It’s also possible to access subsidies that could leverage lower repayments too.

However, these forms of loans carry higher levels of risk for the lenders, and due to this, there are some strict criteria to meet before qualifying for your guaranteed loan and receiving your money.

8. Incubators

Incubators and accelerators are programs that are designed to rapidly scale and build-up startups that show promising growth potential. These programs offer excellent levels of mentoring and seed investments in return for equity in the business.

As an entrepreneur, the mentoring levels offered by incubators and accelerator programs can be invaluable ways of securing growth and sidestepping any potential issues further down the line. The programs offer structured training and the expertise available can really help in developing your business.

However, much like guaranteed loans, the application and selection process can be arduous, and may not be worth persevering with if you’re in need of a cash injection sooner rather than later.

9. Enterprise Investment Schemes

The Enterprise Investment Scheme (EIS) is a tax-efficient way of securing funds that are backed by the HMRC. To a similar effect, Seed Enterprise Investment Schemes (SEIS) can also bring startups some short-term financial joy in the form of specialist loans. When investors subscribe for shares in your business through EIS or SEIS, they can get tax back along with further income relief should they ultimately make a loss on their investment.

The best thing about EIS and SEIS schemes is that they can make your business a much more appealing option for investors due to the government-imposed safety nets in place. This means that more people can be persuaded to part with their money and place it into your endeavour.

Again, with EIS and SEIS, there are plenty of hoops for entrepreneurs to jump through. Terms and conditions can be strenuous and businesses will need to carry out a ‘qualifying trade’ to be accepted onto the schemes.

10. Short-Term Loans

Short-term loans are an altogether riskier option for entrepreneurs to take. Sometimes known as payday loans, short term loans offer quick injections of money into a business to improve working capital, give cash flow a boost or to kick off a new project.

As long as you are confident that you’ll have the funds to make timely repayments, this approach can be highly beneficial – although it’s uncommon to receive significant windfalls in the form of short-term loans.

The best thing about short-term loans is that the funding process can be extremely quick and simple, with many providers offering near-instant payments and fewer regulatory checks along the way.

However, this form of loan comes with extremely high-interest rates, and if you’re unable to make a repayment on a specified date, the penalties involved could become crippling to your startup.

When it comes to taking out loans, always remember to only ever receive money that you believe you’ll be able to repay at the pre-agreed dates. Your startup may be in dire need of cash, but it’s not worth ruining your credit ratings and relationships in order to struggle on with your endeavour. Always run cash flow forecasts to better understand the need for loans, how much will help, and how you’ll plan to pay it back.

The best startups always make sure they keep their books in order as a priority. Strong financial management is the cornerstone of small business prosperity.