If you’re reading this post, it’s probably because you or someone you know has a business plan down to a T. Perhaps you’ve prototyped some products, or have tested the market and have prepared a product launch. Wherever you’re at in your preliminary startup phase, you’ll need a source of capital to fund a scalable business. Startup costs are immediately incurred during the process of planning a business model. From the cost of creating a business plan and research expenses, to employee and marketing overheads. Even the most cost-effective small business needs cash.

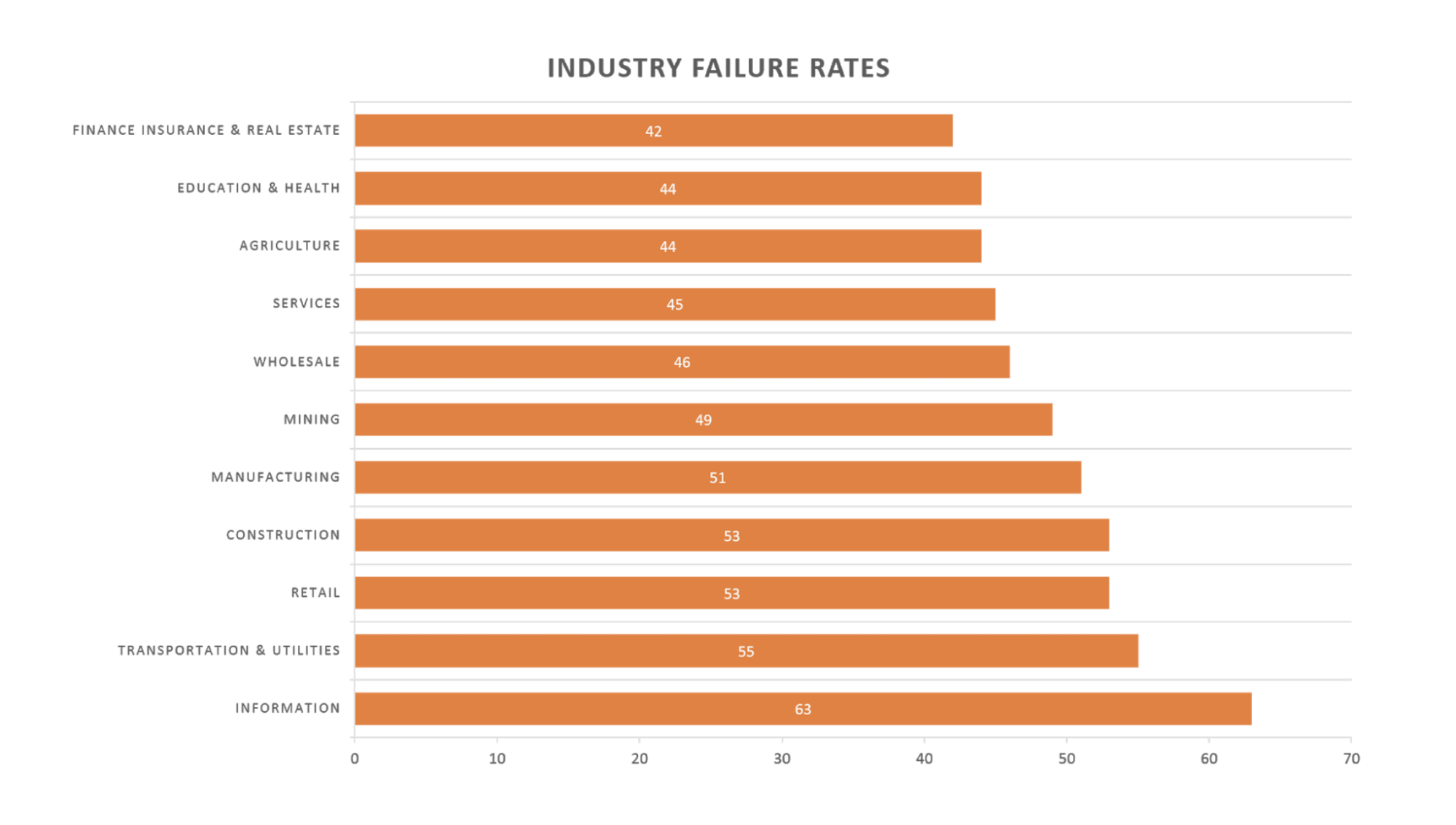

(Startup failure rate by industry. Image: Startup Genome 2019 report)

Across all industries, startup businesses struggle to survive. In fact, only 89% of all startups survive their first year. Going forward, to avoid going under, access to cash has been amongst key prerequisites for growth and success.

The good news is that there are quite a few finance avenues through which entrepreneurs can find sources of capital. Finding the right source for your business could make the difference between ensuring its growth or seriously hindering your progress. Bootstrapping in the early stages of a small business is a good way to avoid debt, proudly raise funds and manage costs through your cash flow.

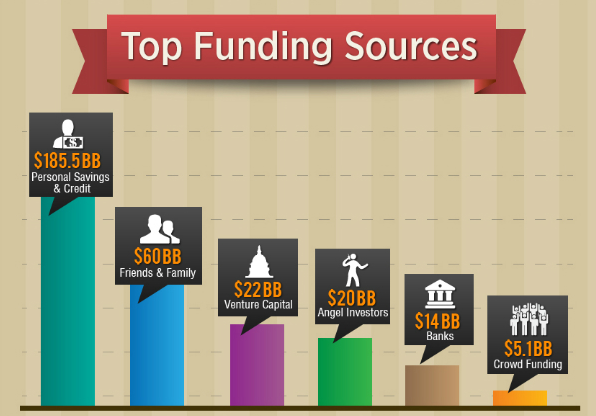

Whilst a staggering 77% of small businesses rely on personal savings for their initial investment, many entrepreneurs will need additional rounds of funding. They might turn to family and friends, angel investors, government grants, venture capital firms or online crowdfunding platforms. Whichever the preferred method, I can assure you, there are pros and cons to them all. So, let’s look at the funding options available for small businesses.

Bootstrapping

For the self-starters; bootstrapping refers to starting your own business and building it with the financial support of your own back pocket. You don’t need millions to successfully bootstrap your way there. Simply get your hands on enough cash to get you started and manage the incurring costs through your cash flow.

(Small business funding sources. Image: Niel Patel)

Bootstrapping has led the way in funding small businesses. Entrepreneurs have a number of options when it comes to putting together sufficient funds. Of course, this varies between entrepreneurs but most will typically aim to save a percentage of their monthly income from a day job, dip into savings, or take out a personal loan.

This admirable approach means entrepreneurs missout on the sizable windfall that can be provided by investors – but their business can grow organically and operate solely under the management of a single business owner. Cash raised, or debt owned effectively belongs to the entrepreneur – meaning they can develop their small business by naturally managing growth without having to play to the pressures of outside capital sources.

Pros of bootstrapping

- Control

- Little to no bureaucratic obstacles

- Little debt

- Learn more about your industry

The most compelling reason to bootstrap your business is to maintain full control over your startup. Consider this, alternative funding sources could promise your £200,000 for example, in return for a 30% stake in your company. Sure, such a significant amount could drastically help you grow your business. However, if your business attains a future market value of £500,000 at any point – £150,000 of this valuation would belong to your external investor.

Many entrepreneurs are drawn to the appeal of having little or no debt when getting a startup off the ground. Since they won’ be accepting lumps of cash from external sources, they can move forward with their own financial balance-sheets to think about – without having to repay investors in the future. There are also fundamentally fewer bureaucratic hurdles to overcome when your finances are your own.

One of the most understated reasons to opt for bootstrapping is that the process of doing so, helps entrepreneurs to learn key lessons about the industry and their business’s place within it. There is no doubt that bootstrapping requires a lot of work but this will pay off in the long run when you are able to call on your experience when it comes to scaling your business.

Cons of bootstrapping

- Limited financial resources

- You’re alone

- Hard work

- You’ll need to multi-manage

- Harder to expand

The most obvious downside to bootstrapping is the looming and imminent danger of struggling to keep operating. Since financial resources are limited to individual entrepreneurs’ capacity, there is no scope to reach out to an external source for additional support. Many small businesses (large businesses too) are forced to fold due to revenue streams drying up. When this is the case for bootstrappers – many feel obliged to sell assets in an attempt to keep their business afloat.

Having an additional source of capital on hand, like a business angel, for example, also provides convenient access to what is usually an expert in the industry. Bootstrappers find themselves alone without the prospect of gaining outside help. Full control of the business has a multitude of benefits, but often a little support can go a long way – especially for inexperienced entrepreneurs.

It’s undeniably hard work, all of which, will be your own. It’s likely that you’ll have to exert extreme caution and exhaust much of your time and energy when it comes to budgeting. A double-edged sword like staff recruitment can be difficult to manage. You’ll have to fork out competitive salaries because there is no room for hiring people who aren’t fit for the role. Without heads of different departments, you’ll find yourself spread across many areas – from marketing, HR and media relations to accounting, finance and sales.

Venture Capital

If your small business has high growth potential or can demonstrate high growth, it’s always possible to pitch your business to Venture Capital (VC) firms to obtain a wealth of financial and professional support in exchange for a share of your company’s equity.

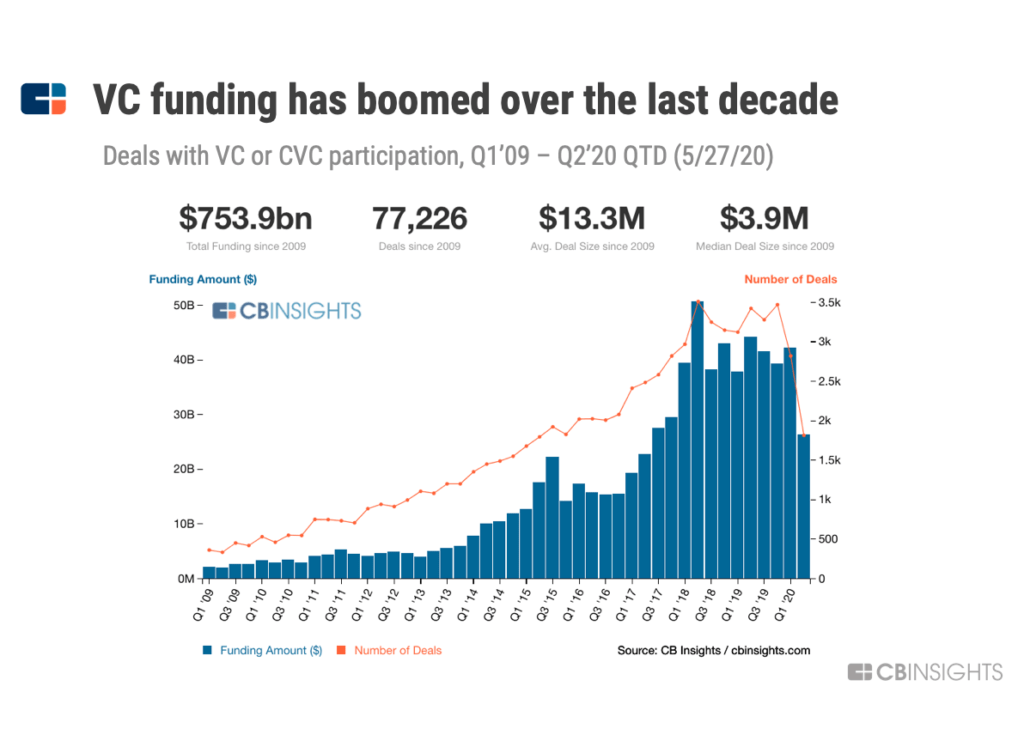

(VC funding 2009 – 2020. Image: CSS Partners)

Don’t be discouraged to seek out VC support if your business is still in its infancy. Micro Venture Capital is money invested in seed early-stage emerging companies with an amount that is typically less than that of traditional venture capital.

The cost of VC is the shares in your company which often transpired into a level of ownership given up. This can range from as little as 1-5% up to 50% and more. For many, this is the major concern with VC funding. The idea of relinquishing ownership initially sounds like a negative. However, it does come with some invaluable benefits.

Pros of VC funding

- Access to significant sums

- Acquire knowledge and industry connections

- You don’t have to repay the money

- Relatively easy to find

There’s no doubt that VC’s can provide an immediate source of large sums that can significantly help a business grow. Closing a deal with a Venture Capitalist enables you to immediately put their cash to good use. Scale-up, grow and expand at a pace that wouldn’t be attainable with minute funding.

A typical VC firm manages, on average, $270 million in venture capital for its investors each year. This capital is typically spread across 30-80 small businesses. Along with a significant cash injection, entrepreneurs gain great levels of guidance from VC’s and are able to benefit from their industry experience, contacts and expertise.

Compared to Angel investors, Venture Capital firms are everywhere and are relatively easy to find. All you need is the ability to demonstrate high growth potential to get them listening and investing.

Cons of VC funding

- Loss of ownership

- Loss of control

- Time lags can set your business back

- Negotiating legal terms

Of course, the biggest downside to VC is the loss of shares in your company that could be felt later on. When your business becomes successful and you consider selling – the money will have to be scaled down to represent your smaller share of the equity. Before reaching out to a VC firm, consider whether a percentage of equity is worthy of the cash you’ll receive now.

More shareholders in a company mean that more people will have a say in any decision making process. Often, VC’s will have a strong say in the use of the capital, expansion plans and other operating considerations. The decision to take your business in a particular direction is no longer solely the entrepreneurs’.

The time it takes to reach out to a VC firm, pitch your case and close a deal, can set a business back. If it’s a case of finding capital to fund a new project or expand in a new market – these endeavours can wait it out. For small businesses that need funding immediately to save them from going under – VC might not be appropriate.

Angel investors

Angel investors are essentially high-net-worth individuals who invest their own money in promising ventures. For angels, these investments tend to not be as lucrative as those of Venture Capital, but angels have been known to financially support risky ventures. Above all, angel investors are more likely to invest in a company operating within their expertise or field of interest.

They provide capital in exchange for convertible debt or ownership equity. Just like the businesses they back, angel investors come in all shapes and sizes. Angels tend to be relatively more hands-on with the businesses they support than other investors. They give their time, skills, contacts and business knowledge to entrepreneurs.

In the UK alone, angels invest £1.5bn each year into small businesses (UK Business Angels Association). To shed light on this financial scale – that is three times the amount invested by venture capitalists. Without belonging to organizations, Angel investors are regulated by the Financial Conduct Authority to protect investors and businesses. They ensure that angels cannot take more than a 30% share of the business they invest in.

To be an appealing investment opportunity, you should own a profitable early-stage business and have an annual turnover of up to £5 million. You should also be in need of between £15,000 and £500,000. The last prerequisite is to be willing to hand over a share of your business and expect to work closely with your angel.

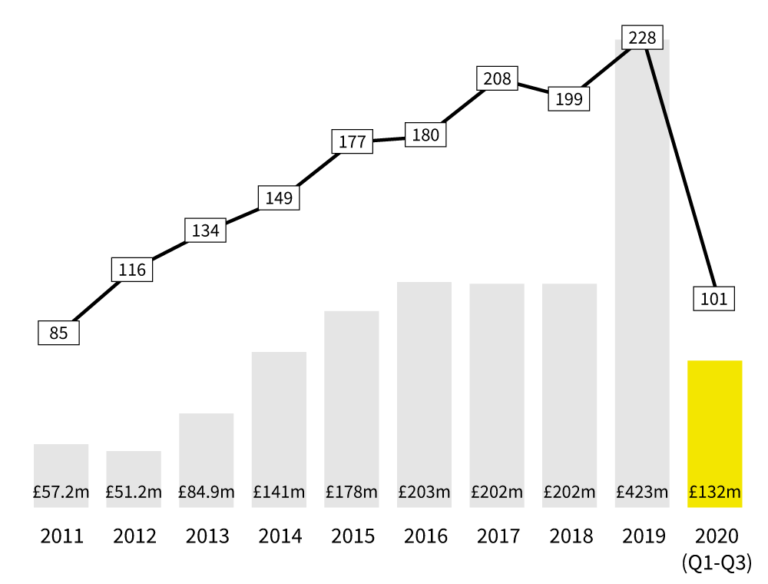

Angel investment into UK companies over time

(Angel investment into UK companies 2011 – 2020. Image: Beauhurst)

Pros of Angel Investors

- They have an investor network

- Well versed in business development

- They have equity to spare

These well-established entrepreneurs-come-investors know a good investment opportunity when they see one. Unlike banks, they’re not afraid to throw cash at an idea that they think has potential. Their spare equity sets them apart from banks who have major concerns about repayments and little concerns over the health or expansion of your business.

Angel investors know other angel investors. Their network enables them to bring each other in on particular opportunities, raising more capital for a small business and generating a wealth of experience and knowledge to lean on.

Cons of Angel Investors

- There are strings attached

- Pressure to deliver

- Loss of control

Entrepreneurs aren’t technically obligated to repay the angel investor the money they inject. However, handing over equity in the company is part of the deal and means that an entrepreneur is instantaneously giving away part of their future net earnings. When the offer is on the table, review the terms carefully to make sure that the amount of equity the angel investor is requesting doesn’t impact your ability to profit.

Angels’ high-risk tolerance often translates into expectations of high returns. In fact, it’s not uncommon for an angel investor to expect a rate of return that is up to 10 times the amount of their initial cash-injection within the first 5 years. Not meeting these expectations could result in no more funding from them in the future.

High risk also means that most angels will want partial control over a company they invest in. Even when the reins are left to the entrepreneur, they may at the very least, have to explain their decisions to their angel investor.

Small business grants

Governments and institutions provide a number of small business grants to entrepreneurs across all industries. The nature of grants can range from cash rewards to tax reliefs with the aim of stimulating entrepreneurial activity and growth.

Cash grants, unlike loans, do not need to be repaid and as such, are amongst the most desired sources of funding for small businesses. No active force of an investor means that qualifying entrepreneurs take the cash and their business in the direction of their choice.

Direct grants are essentially a cash sum awarded to a small business to either cover startup costs like training, research, manufacturing and marketing, or to fund a very specific project. Typically, the entrepreneur will be required to raise and provide 50% of the grant value. When a grant is requested for a particular project, there are often conditions attached to how the money is spent.

Pros of small business grants

- The money needn’t be repaid

- Attract additional rounds of funding in the future

The main benefit of a small business grant is that the money doesn’t need to be paid back to the institution and small business owners don’t need to part with any equity. As such, the business owner retains full control of the company.

Those who adhere to the conditions of a small business grant – in the case of using the grant for a project, for example – are able to demonstrate their ability to manage money and show results. This can work in an entrepreneurs favour when it comes to reaching out to investors in the long run.

Cons of small business grants

- Highly competitive

- It can take time to receive the cash

- Terms and conditions applied

There’s no question that small business grants are the most demanded source of funding for small businesses. As a result, they are highly competitive and small businesses should be able to demonstrate their high potential and unique place in the market.

If you’re lucky enough to get your hands on a small business grant, the process between applying for one and receiving the grant can be timely. Waiting to hear back from an application that could be declined can put pressure on already struggling small businesses. Not to mention the additional terms and conditions that put further pressure on the small businesses that are actually awarded the grant.

Crowdfunding

Tap into the vast potential of the internet to find funding for small businesses. Crowdfunding is a relatively time-efficient and inexpensive way to secure capital for a business idea, product launch or particular project. It also helps small businesses connect with their most interested target customers.

Crowdfunding is a straightforward process which invites a large number of investors to contribute a relatively small amount of money to a small business. There are plenty of dedicated platforms out there that enable small business owners to build business profiles. Websites like Seedrs and Crowdcube are popular places for small businesses seeking funding.

Traditional crowdfunding promises investors special gifts, promotions and discounts on products and services, while equity crowdfunding is focused on investing in a business in return for future profits. Interestingly, those who benefit most from crowdfunding have been found to be female entrepreneurs. A report from the PwC and the Crowdfunding Center found that women are 32% more likely to reach their crowdfunding goals than men. Whilst this shouldn’t discourage men from attempting to raise capital from crowdfunding, women who are struggling to find funding from alternative sources may well be able to do so through crowdfunding.

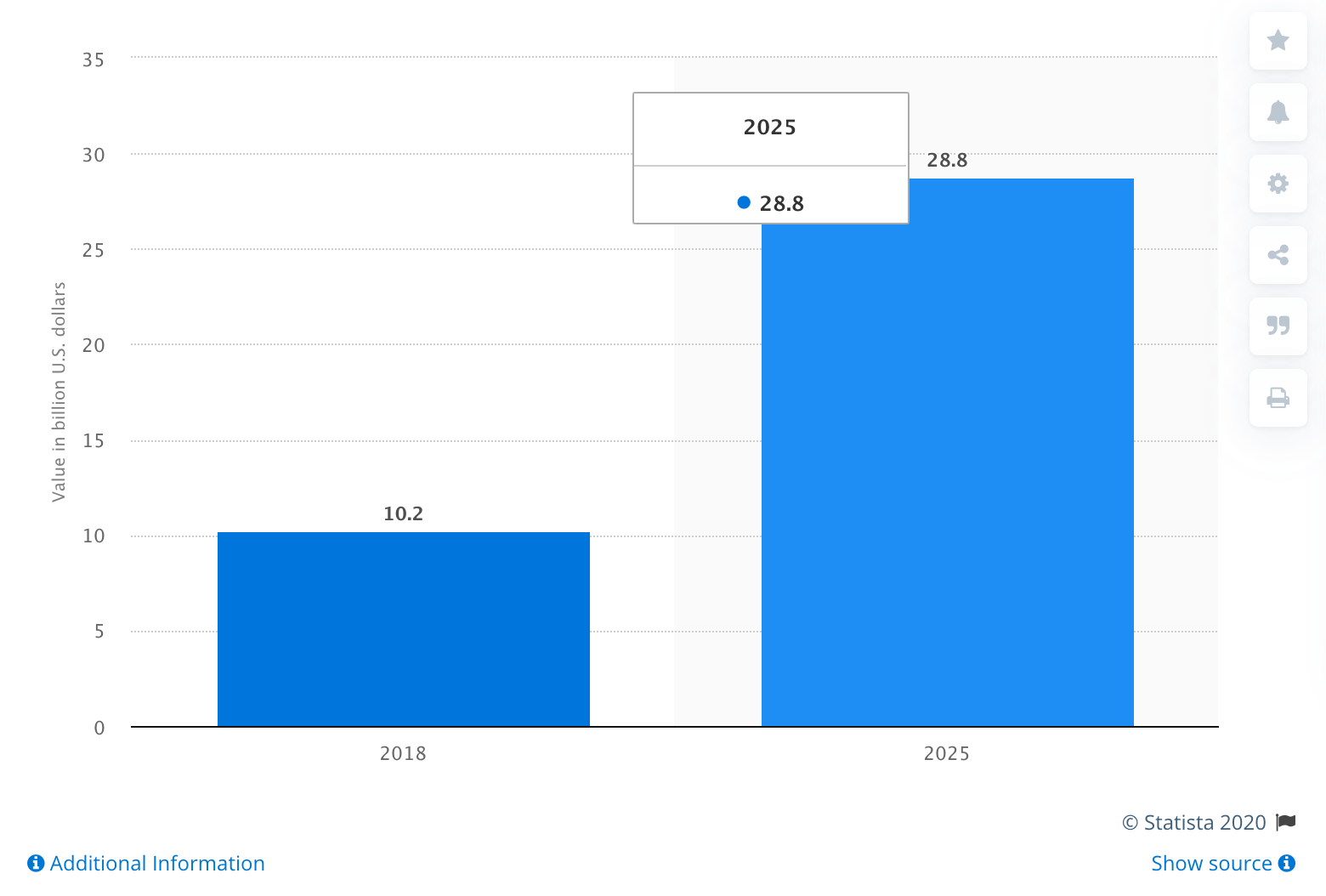

Crowdfunding market forecast to triple by 2026

(The projected market size of crowdfunding worldwide. Image: Statista)

Pros of crowdfunding

- Brand awareness

- Form customer relationships

- You may not need to repay the money

Crowdfunding is by far the cheapest way for small businesses to secure funding. Reward-based crowdfunding, in particular, enables small businesses to attract interest and donations without the need to sell any equity or relinquish control in their business. Few questions are asked about the business plan itself, and lengthy meetings with banks and investors are avoided.

With a global digital population of 4.8 billion people (Statista), the exposure gained on the platform can help to establish brand awareness on the largest scale. What’s more, those who are interested enough to make a donation to a small-business are likely to become customers too. Meaning, small businesses can begin to build relations with their most important target customers.

Cons of crowdfunding

- Amounts raised should reflect awards distributed

- Conditions attached

- Exposure to competition

As per the name, crowdfunding revolves around raising money from the ‘crowd’ and relies on individual donations. Small businesses that are aiming to raise large amounts of money should keep in mind that the value should be reflected in the rewards or future earnings that are given away. This can be a major setback for small businesses that are not capable of doing so.

Most crowdfunding websites have a rigid set of conditions applied to their use. In some cases, if you don’t reach your entire goal – you may have to forfeit the amount of money raised. This can lead to some small businesses understating the amount they need. Others, like Kickstarter, do not allow equity fundraising and have an extensive list of prohibited items that exclude certain campaigns.

Pitching a business idea on a crowdfunding platform, whilst attracts potential donors, also exposes it to competitors. To avoid having business ideas stolen, it’s advisable to protect it with a patent – which costs money.

Friends and family funding

Friends and family rounds of funding are, for many, the first foundational steps of finding funding for small businesses. This type of funding typically comes before seed rounds and is often considered a ‘top-up’ on the capital that an entrepreneur raises themselves. Of course, the extent to which this is possible is highly dependent on each entrepreneur’s individual situation.

In some cases, friends and family may continue to provide further rounds of funding at different stages. However, this network is often surpassed by more sophisticated capital as a small business grows and becomes more attractive to angel investors and venture capitalists.

Pros of friends and family funding

- Easy to raise

- Good financing terms

- Slack when you need it

Getting friends and family to lend you money for a business should be relatively easy. That is – in comparison to producing enticing PowerPoint presentations and working on your credit score. The only prerequisites are that your business idea is sound with reasonable anticipation of success.

Whether you come to debt or equity arrangements, you should hope that these agreements are the most attractive funding terms you can get. Once again, it’s all relative but here’s hoping that your friends and family aren’t all loan sharks.

Friends and family are also more likely to be understanding when things go wrong. Whilst you do everything in your power to limit these instances, sometimes the pressure is eased when you know you don’t have to report back to the bank manager, or highly demanding venture capitalist.

Cons of friends and family funding

- Limited capital

- Relationship risk

- Future implications

Unless you descend from a family of billionaires, you will have access to a limited amount of capital. Sooner or later you will need to tap into other sources of funding. Whilst this might be reasonable for early-stage small businesses, those on a growth trajectory might require larger sums of capital to accommodate their expansion plans.

Should your venture fail, or your daily and friends feel they aren’t getting the rewards and benefits they deserve, relationships can become strained. This can have devastating impacts on both your small business as well as your relationships. Consider carefully whether you are willing to put your relationships on the line for financial backing.

Remember that each round of funding can and does have ripple effects on the next. If a small business acquires a lot of debt at high rates with family or gives up large chunks of equity early on – it can significantly dampen future fundraising efforts.